Can a Dealership Take Back a Car After Payment?

Buying a car is a big step, and sometimes questions pop up after you’ve driven off the lot. A common worry for new car buyers is, “Can a Dealership Take Back a Car After Payment?” It can seem confusing because you’ve paid for it. This guide makes it simple.

We’ll walk you through the reasons why this might happen and what your rights are.

Understanding Car Dealership Take-Backs

This section explains why a dealership might need to take back a car, even after you’ve paid for it. It’s not usually about you changing your mind. Instead, it often involves financing or contract issues.

We will explore the main reasons this situation can occur, making it clear for everyone to grasp.

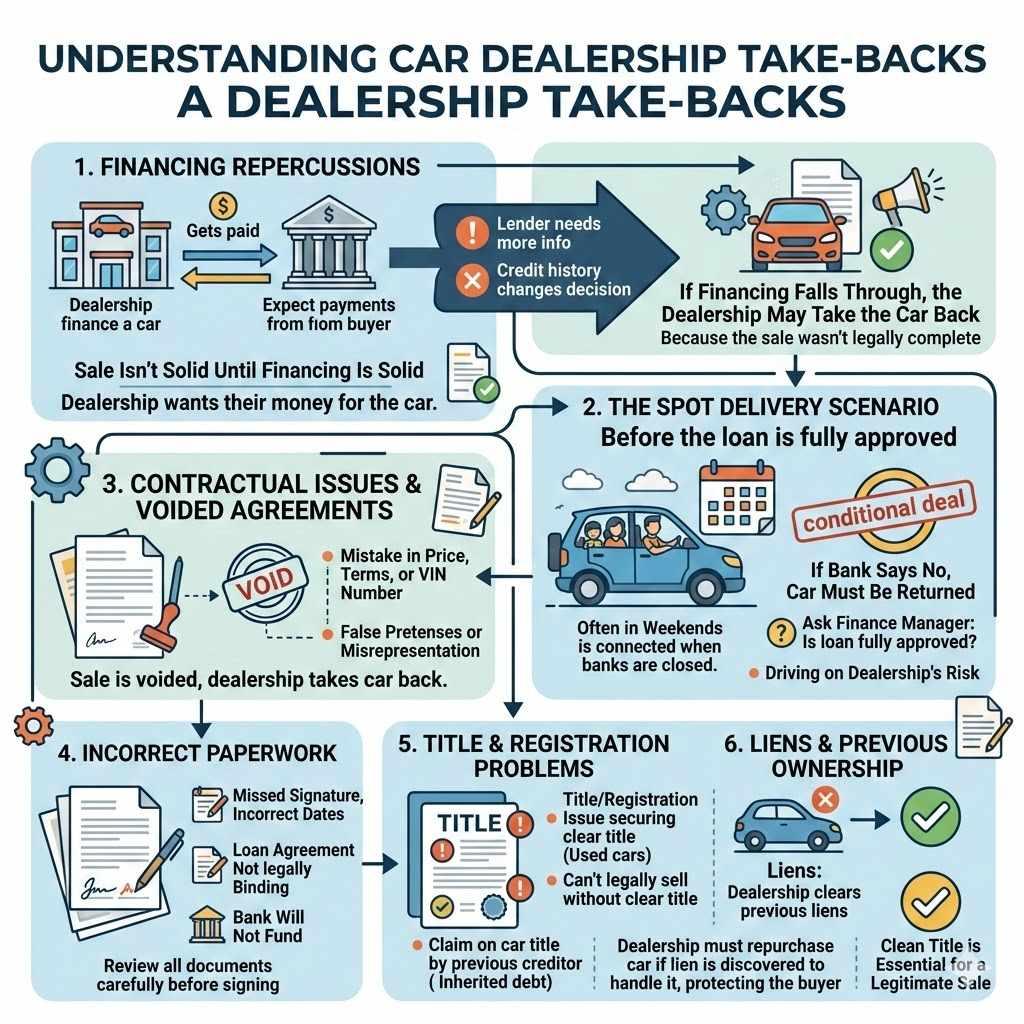

Financing Repercussions

When you buy a car, you often finance it. This means a bank or lender pays the dealership, and you pay the bank back over time. Sometimes, the financing deal isn’t fully approved or finalized.

This can happen for several reasons.

The lender might need more information from you. They might also discover something in your credit history that changes their decision. If the financing falls through, the dealership might have to take the car back because they haven’t truly sold it.

This is a critical point for buyers. If the financing isn’t solid, the sale isn’t solid either. The dealership is on the hook if the bank doesn’t give the loan.

They want to make sure they get their money for the car.

The Spot Delivery Scenario

A common reason for a take-back is a “spot delivery.” This is when a dealership lets you drive a car home before the loan is fully approved. They hope the loan will be approved. If it’s not, they ask for the car back.

This often happens when you buy a car on a Saturday or Sunday. The bank might not be open to fully approve the loan until Monday. The dealership wants your business and might let you take the car to get you excited.

But if the bank says no, you have to return the car.

It’s important to know if your loan is fully approved. Ask the finance manager. A “spot delivery” means the deal is conditional.

You are driving the car on the dealership’s risk until the bank says yes.

Contractual Issues and Voided Agreements

Car sales contracts are legal documents. Sometimes, there are errors or missing information in the contract. These issues can make the contract invalid.

If a contract is voided, the sale cannot stand.

This might happen if there was a mistake in the price, the terms, or even the VIN number of the car. The dealership may have to void the sale and take the car back. This is rare but can occur.

It is also possible that the contract was signed under false pretenses or with misrepresentation. If a buyer can prove this, the contract could be deemed invalid. The dealership would then have to return any payments made and repossess the vehicle.

Incorrect Paperwork

Simple mistakes in paperwork can cause big problems. This could be anything from a missed signature to incorrect dates. These errors can prevent the financing from being finalized.

If the paperwork is not done correctly, the loan agreement might not be legally binding. The bank will not fund the purchase. This leaves the dealership in a difficult position.

They might have to reclaim the car.

It’s good practice to review all documents carefully. Make sure all names, dates, and figures are correct before signing. Ask questions if anything seems unclear.

This helps prevent future issues.

Title and Registration Problems

Getting the car’s title and registration in your name is a key part of the sale. Sometimes, there can be issues with proving ownership or transferring the title. This is especially true for used cars.

If the dealership cannot secure a clear title for the car, they cannot legally sell it to you. They might have to take the car back until they can resolve the title issues. This could happen if the car has a lien on it from a previous owner that wasn’t cleared.

The registration process also needs to be smooth. If there are delays or problems with getting the plates and registration sorted, it can hold up the final sale. The dealership may need the car back temporarily.

Liens and Previous Ownership

A lien is a claim on a property, like a car, by a creditor. If a previous owner owed money on the car, there might be a lien on its title. The dealership must ensure all previous liens are cleared before they can transfer ownership to you.

If a lien is discovered after the sale, and the dealership didn’t handle it properly, they may have to repurchase the car from you. They then have to sort out the lien themselves. This protects you from inheriting someone else’s debt.

This is why dealerships do title searches. They want to be sure they are selling you a car with a clean history. A clean title is essential for a legitimate sale.

Your Rights As A Buyer

Even if a dealership needs to take a car back, you still have rights. Knowing these rights can protect you and ensure a fair process. This part focuses on what protections you have.

Cooling-Off Periods and Rescission Rights

In most places, there isn’t a mandatory “cooling-off period” for car sales, meaning you can’t just change your mind and return the car after payment. However, specific contract terms or state laws might offer some protection.

Some contracts might include a rescission clause. This clause allows you to cancel the contract under certain conditions. It’s very important to read your contract thoroughly to see if such a clause exists and what its terms are.

If the dealership is taking the car back due to financing issues, your contract may state what happens to any money you’ve paid. You should get a full refund if the sale is truly undone.

Contractual Agreements

Your purchase agreement is the most important document. It outlines the terms of the sale. If the dealership agreed to specific terms in writing, they must honor them.

If the contract states the sale is final once payment is made and financing is approved, then the dealership generally cannot take the car back unless there’s a breach of contract by the buyer or a specific clause allowing it.

Always keep copies of all paperwork. This includes the bill of sale, financing agreements, and any communication with the dealership. This documentation is your proof.

Lemon Laws and Vehicle Defects

“Lemon laws” protect consumers who buy vehicles that have serious defects. These laws vary by state. They usually apply when a car has a defect that cannot be fixed after a reasonable number of repair attempts.

If your car turns out to be a lemon, you may be entitled to a refund or a replacement vehicle. This is different from a dealership taking a car back due to financing. This is about the car itself being faulty.

To use lemon laws, you typically need to show the defect happened while the car was under warranty. You also need to show that the dealership had a reasonable chance to repair it. This usually means at least three repair attempts for the same problem.

What to Do If You Believe Your Car Is a Lemon

Keep detailed records of all repairs. Note the dates, the problems described, and the work performed. This documentation is vital.

Communicate clearly with the service department. Make sure they understand the issues. If repairs don’t fix the problem, ask for a written statement from the mechanic.

If you believe your car qualifies as a lemon, you can contact your state’s Attorney General’s office or a consumer protection agency. They can guide you on filing a claim.

Steps To Take If A Dealership Wants Your Car Back

If you find yourself in a situation where a dealership wants to take your car back, it’s important to act calmly and strategically. Here’s a step-by-step approach.

Review Your Contract Immediately

Your purchase agreement is the first place to look. It contains all the terms and conditions of your sale. Pay close attention to any clauses about financing, cancellations, or “spot deliveries.”

Look for specific language that might allow the dealership to take back the car. Also, check for any clauses that protect you. This document is your primary guide.

If you’re unsure about what a clause means, do not hesitate to seek legal advice. A small consultation fee is better than losing your car and money.

Communicate Clearly With The Dealership

Ask for a clear explanation in writing. Why do they want the car back? What specific part of the contract or financing is the issue?

Get all communication in writing.

Do not feel pressured to return the car immediately. Ask for time to review the situation and consult with others if needed.

Be polite but firm. State your understanding of the agreement and your rights.

Seek Legal Advice If Necessary

If you feel the dealership is acting unfairly or you don’t understand your rights, consult a lawyer. An attorney specializing in consumer law or automotive disputes can provide expert guidance.

A lawyer can review your contract and advise on the best course of action. They can also help negotiate with the dealership on your behalf.

Many lawyers offer a free initial consultation. This can be a good way to understand your options without immediate cost.

Preventing Dealership Take-Backs

The best way to handle situations where a dealership might take back a car is to prevent them from happening in the first place. This involves being diligent during the purchase process. We’ll cover key strategies.

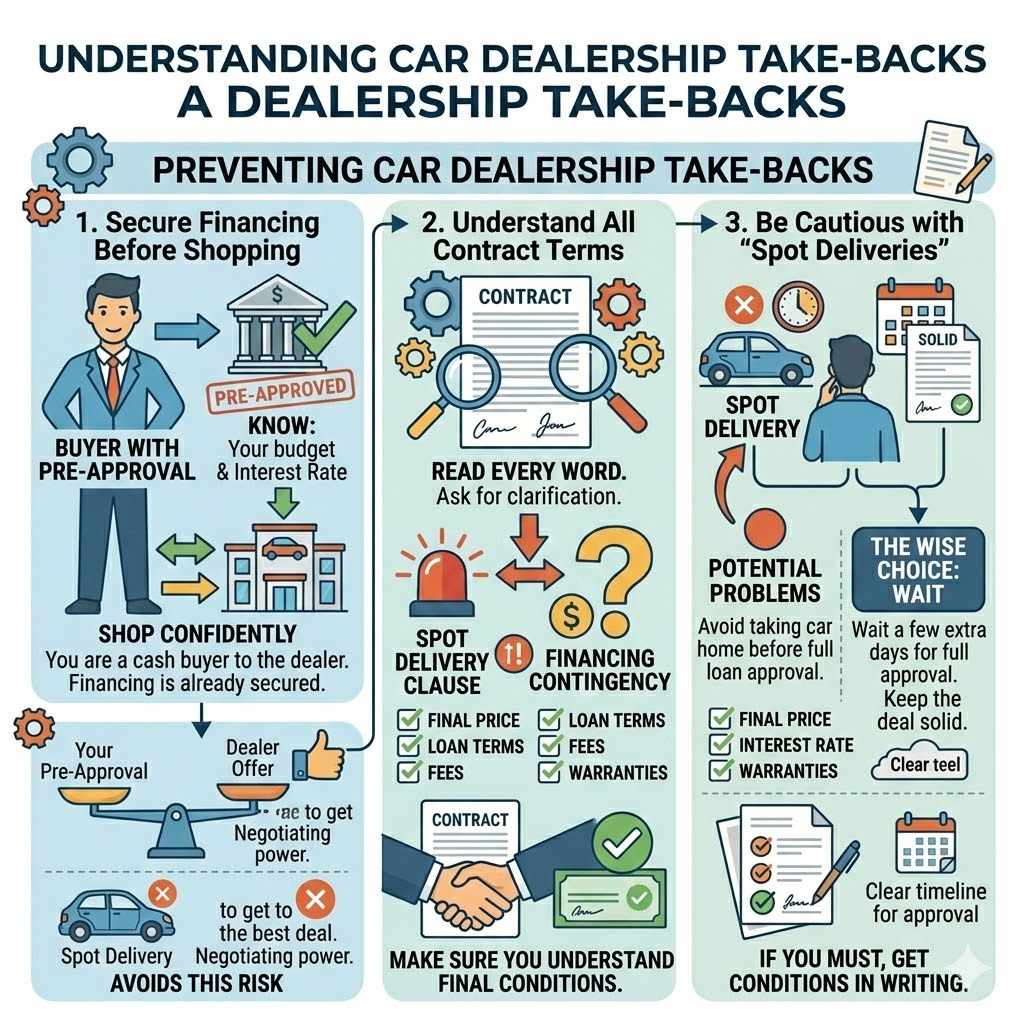

Secure Financing Before Shopping

The most proactive step is to get pre-approved for a car loan from your bank or credit union before you visit a dealership. This way, you know exactly how much you can borrow and at what interest rate.

Having pre-approval means you are a cash buyer to the dealership. They know the financing is secured. This removes the risk of a “spot delivery” gone wrong.

It also gives you negotiating power. You can compare dealership financing offers to your pre-approval to ensure you are getting the best deal.

Understand All Contract Terms

Before signing anything, read every word. If a term is confusing, ask for clarification. Don’t let the salesperson rush you through the paperwork.

Pay attention to the “out” clauses, like a “spot delivery” clause or a financing contingency. These are critical. A financing contingency means the sale is dependent on loan approval.

Make sure you understand the final price, interest rates, loan terms, and any added fees or warranties.

Be Cautious with “Spot Deliveries”

While dealerships may offer to let you take a car home before final financing approval, it’s often best to wait until everything is ironed out. This avoids potential problems.

If you do take a car on a “spot delivery,” ensure you have a clear understanding of the conditions and the timeframe for final loan approval. Get this in writing.

If the dealership insists on a spot delivery, you might consider if you really need the car that urgently. It might be wiser to wait a few extra days for full approval.

Frequently Asked Questions

Question: Can a dealership take back a car after I’ve made a full cash payment?

Answer: Generally, no. If you pay for the car in full with cash and all paperwork is complete, the sale is final. The dealership cannot take it back unless there’s a significant issue with the title or registration that they failed to disclose, or a clause in a specific contract allowing it, which is highly unusual for a cash sale.

Question: What if the dealership lied about the financing approval?

Answer: If a dealership intentionally misled you about financing approval to get you to sign a contract, this could be considered fraud. In such cases, you likely have legal recourse. You should consult with a consumer protection lawyer to understand your options.

Question: How long does a dealership typically have to take a car back if financing falls through?

Answer: This depends heavily on the contract and state laws, but often it’s very soon after the financing is definitively denied. Dealerships usually want to resolve these issues quickly. The contract should specify the timeframe or conditions under which a “spot delivery” can be rescinded.

Question: Can I get my trade-in back if the dealership takes back the new car?

Answer: If the dealership takes back the car you purchased, your original trade-in should also be returned to you, assuming it hasn’t been sold. If your trade-in has been sold, the dealership would likely owe you its market value or the agreed-upon trade-in value, whichever is higher, in addition to any payments you made on the car being returned.

Question: What if I made modifications to the car before the financing was finalized?

Answer: If you made modifications to the car before financing was finalized and the dealership needs to take it back due to financing issues, you may be responsible for returning the car to its original condition. Any costs associated with removing the modifications or repairing any damage caused by them could fall on you. It’s best to avoid modifications until the sale is fully complete and secure.

Summary

A dealership taking back a car after payment is usually tied to financing issues, not buyer’s remorse. Key reasons include loan denials, spot deliveries, or contract problems. You have rights, especially regarding clear titles and vehicle defects.

Always review your contract, get pre-approved for loans, and communicate in writing to prevent these situations and protect your purchase.