Does Mastercard Have Car Rental Insurance? Vital Guide

Yes, many Mastercard cards offer built-in auto rental collision damage waiver (CDW) or loss damage waiver (LDW) coverage as a cardholder benefit, but it typically has specific terms and conditions. This can potentially save you money by letting you decline the rental company’s expensive insurance.

Renting a car often feels like an adventure, but when you get to the counter, the insurance options can be a bit overwhelming. The rental company might offer you their Collision Damage Waiver (CDW) or Loss Damage Waiver (LDW). These can add a significant amount to your daily rental cost. But before you say “yes” to that extra charge, did you know your trusty Mastercard might already have you covered? It’s a smart benefit many travelers overlook. This guide will help you understand if your Mastercard offers this valuable perk and how to use it properly.

Understanding Car Rental Insurance: What You Need to Know

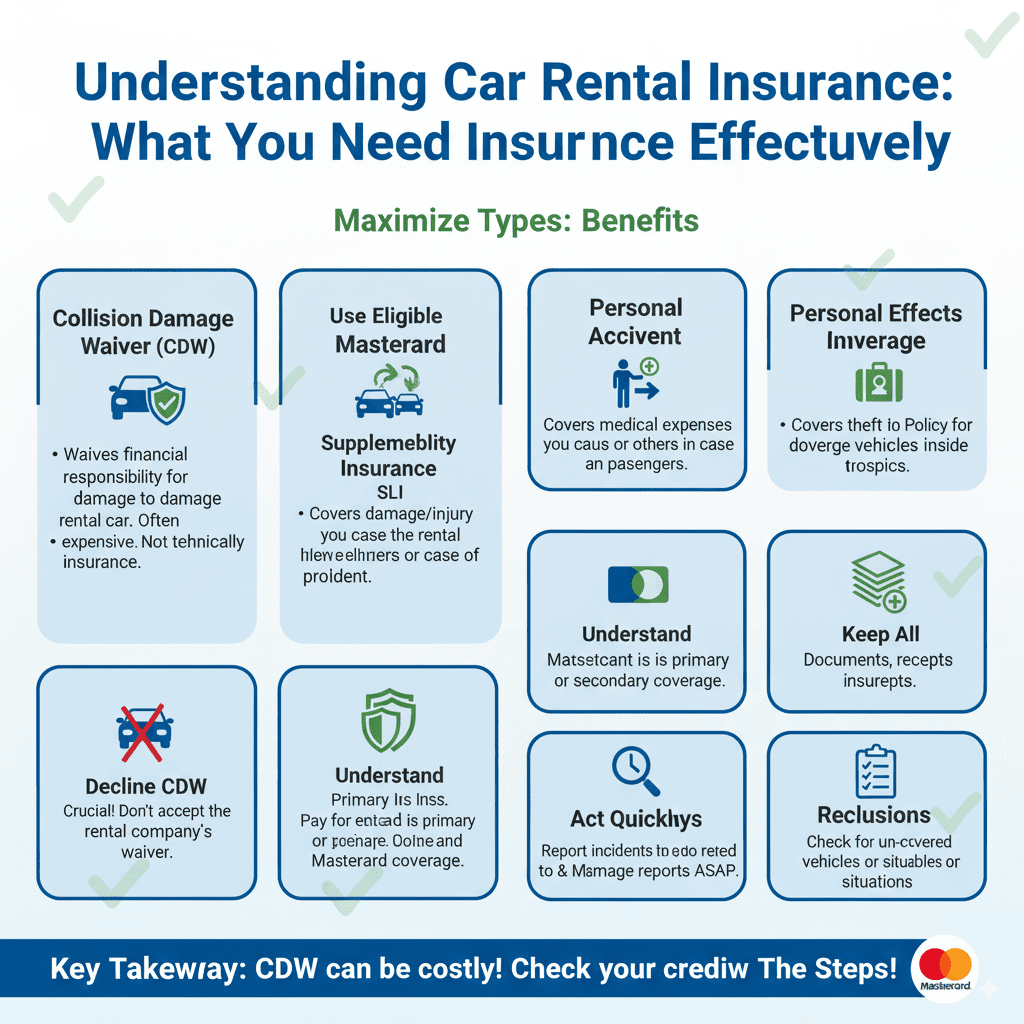

When you rent a car, the rental company will present you with several insurance options at the counter. The most common ones are:

- Coverage for Damage to the Rental Vehicle: This is usually called a Collision Damage Waiver (CDW) or Loss Damage Waiver (LDW). It essentially waives your responsibility for damage that occurs to the rental car. It’s not technically insurance, but it acts like it by releasing you from financial liability for damage.

- Supplemental Liability Insurance (SLI): This covers you if you cause an accident and injure someone or damage their property.

- Personal Accident Insurance (PAI): This covers medical expenses for you and your passengers in case of an accident.

- Personal Effects Coverage (PEC): This covers theft or damage to your personal belongings inside the rental car.

The CDW/LDW offered by rental companies can be quite expensive, often ranging from $15 to $30 or more per day. While it provides peace of mind, it’s worth investigating if your credit card already offers similar protection.

Does Mastercard Offer Car Rental Insurance?

This is the big question! The good news is that many Mastercard credit cards do provide valuable auto rental insurance benefits. This is typically offered as a Collision Damage Waiver (CDW) program. It’s important to know that this benefit is usually secondary coverage, meaning it kicks in after any primary insurance you might have (like your personal auto insurance or credit card’s primary insurance). However, for many renters, this secondary coverage is sufficient.

Here’s what you need to understand about Mastercard’s car rental insurance:

- It’s a Benefit, Not a Standalone Policy: This coverage is a perk of using your Mastercard. It’s not something you purchase separately from the rental company.

- It’s Typically a CDW/LDW: The primary benefit offered is coverage for damage or theft to the rental vehicle itself. It usually doesn’t cover liability to other parties.

- Coverage Varies by Card Tier: The level of coverage and specific terms can differ significantly depending on the type of Mastercard you have. Premium cards (like World Elite Mastercard or World Mastercard) often have more robust benefits than standard Mastercard cards.

- You Must Decline the Rental Company’s CDW/LDW: To activate your Mastercard’s benefit, you must use your eligible Mastercard to pay for the entire rental and explicitly decline the CDW/LDW offered by the rental company.

How Mastercard’s Auto Rental CDW/LDW Works

Mastercard’s Auto Rental CDW/LDW is designed to reimburse you for eligible damages to a rental vehicle up to a certain amount. Here’s a general breakdown of how it typically functions:

- Choose Your Eligible Mastercard: Make sure your Mastercard is one that offers this benefit. You can usually find this information on your card issuer’s website or by calling their customer service.

- Book and Pay with Your Mastercard: Use your eligible Mastercard to reserve and pay for the entire rental transaction. This step is crucial for coverage to apply.

- Decline the Rental Company’s CDW/LDW: At the rental counter, politely decline the Collision Damage Waiver (CDW) or Loss Damage Waiver (LDW) offered by the rental agency.

- Drive the Rental Car: Enjoy your trip!

- In Case of Damage or Theft: If the rental car is damaged or stolen during your rental period, you will first be responsible for settling the claim with the rental company.

- Initiate a Claim with Mastercard/Your Issuer: Contact your credit card issuer’s benefits administrator (often a third-party company) as soon as possible to start the claim process. You will need to provide documentation, such as the rental agreement, police reports (if applicable), and damage estimates.

- Reimbursement: If your claim is approved, the Mastercard CDW/LDW will reimburse you for the covered damages, according to the policy limits and terms.

Key Requirements and Limitations to Be Aware Of

While Mastercard’s auto rental CDW/LDW is a fantastic benefit, it’s not a universal, no-questions-asked coverage. There are specific rules and limitations you absolutely must understand to ensure you are covered. Ignoring these can lead to your claim being denied.

Eligible Rentals and Vehicles:

Mastercard’s coverage usually applies to:

- Most standard rental cars (sedans, SUVs, etc.).

- Rental periods for a limited number of consecutive days (often 30 or 31 days).

However, coverage is often excluded for:

- Luxury, exotic, or antique vehicles.

- Certain types of vehicles like large trucks, vans seating more than a certain number of passengers, RVs, and motorcycles.

- Rentals outside of your country of residence (though some premium cards may offer coverage abroad).

- Vanpooling or off-road use.

Coverage Limits:

There’s usually a maximum amount that will be reimbursed for damage or theft. This limit is often around $50,000, but it can vary. This limit is generally quite high and sufficient for most common rental car damages.

Primary vs. Secondary Coverage:

This is a critical distinction. Most Mastercard rentals CDW/LDW benefits are considered secondary coverage. This means:

- If you have other insurance: Mastercard’s coverage will only apply after your primary insurance (like your personal auto insurance policy, if it covers rentals, or your credit card’s primary rental insurance, if offered) has paid out its portion.

- If you do NOT have other insurance: In some cases, the coverage might function as primary for the rental car itself. However, you MUST verify this with your specific card issuer.

Why is this important? If your personal auto insurance is triggered, it could lead to a premium increase. Using Mastercard’s secondary coverage first can help avoid this if your personal insurance doesn’t cover rentals or if you want to avoid a claim on your personal policy.

Documentation Requirements:

To file a claim, you’ll need to provide a significant amount of documentation. Be prepared to gather:

- A copy of the rental agreement.

- Receipts showing the full rental cost paid with your Mastercard.

- The final bill from the rental company when you returned the car.

- A police report, if one was filed after an accident or theft.

- Repair estimates or invoices from the rental company.

- Any other documents requested by the benefits administrator.

The claims process can be lengthy, so patience and thoroughness are key.

Exclusions:

Common exclusions for Mastercard’s CDW/LDW include:

- Damage due to negligence (e.g., running out of gas, driving under the influence).

- Tire, windshield, or other damage that the rental company may try to attribute to misuse rather than an accident.

- Loss of use fees charged by the rental company while the car is being repaired.

- Diminution of value (the rental company’s claim that the car is worth less after being damaged, even if repaired).

- Theft if keys are left in the vehicle or the vehicle is left unlocked.

- Damages from driving on unpaved roads or in areas not intended for vehicular travel.

Comparing Mastercard CDW/LDW to Other Options

It’s helpful to see how Mastercard’s benefit stacks up against what rental companies offer and your personal auto insurance.

| Coverage Option | Typical Cost | What It Covers | Pros | Cons |

|---|---|---|---|---|

| Mastercard Auto Rental CDW/LDW | Included as a card benefit (no extra daily charge) | Damage/theft to rental car (up to policy limit) | Saves money vs. rental company waiver. Convenient. May be primary for some cardholders. | Usually secondary. Specific vehicle/rental exclusions. Requires declining rental coverage. Can have a complex claims process. |

| Rental Company CDW/LDW | $15 – $30+ per day | Damage/theft to rental car. Often waives “loss of use” and “diminution of value.” | Easy to purchase. Often covers more “gaps” like loss of use. May be primary coverage. | Very expensive. Can be confusing with different waiver types. |

| Personal Auto Insurance | Varies (if covered under your policy) | Coverage depends on your policy terms (often covers damage, liability). | Might be primary. Familiar terms. Can cover a wider range of vehicles. | May increase your premiums if used. Deductible applies. Might not cover all rental situations (check your policy!). |

| TPL/SLI Insurance (from Rental Company) | $10 – $20+ per day | Liability for damage to other vehicles/property and injuries to others. | Provides crucial liability protection if your personal insurance is insufficient or unavailable. | Adds significantly to daily cost. |

As you can see, the Mastercard benefit offers significant cost savings. However, it’s vital to understand its limitations, particularly whether it’s primary or secondary for your specific card.

How to Verify Your Mastercard’s Coverage

Not all Mastercard cards come with auto rental insurance. The benefit is typically tied to specific card tiers like World Mastercard and World Elite Mastercard. Even then, the exact terms can be set by the bank that issued your card.

Here’s how to find out for sure:

- Check Your Cardholder Agreement: This is the most authoritative source. Look for sections on “Auto Rental Insurance,” “Collision Damage Waiver,” or similar terms.

- Visit Your Card Issuer’s Website: Log in to your online account. Most issuers have a dedicated “Benefits Guide” or “Perks” section for each card.

- Call the Customer Service Number on Your Card: Ask the representative specifically about “Auto Rental Collision Damage Waiver” benefits for your card number.

- Look for a Benefits Administrator Number: Sometimes, Mastercard or your issuer will list a separate phone number for its auto rental insurance benefits administrator. Calling this number can connect you directly with the experts who manage these claims.

When you call or check online, ask these important questions:

- Does my card offer an Auto Rental CDW/LDW benefit?

- Is this coverage primary or secondary?

- What is the maximum coverage amount?

- What types of vehicles are excluded?

- What is the maximum rental period covered?

- Are there any geographical limitations (e.g., coverage outside the US)?

- What is the phone number for the benefit administrator to file a claim or ask detailed questions?

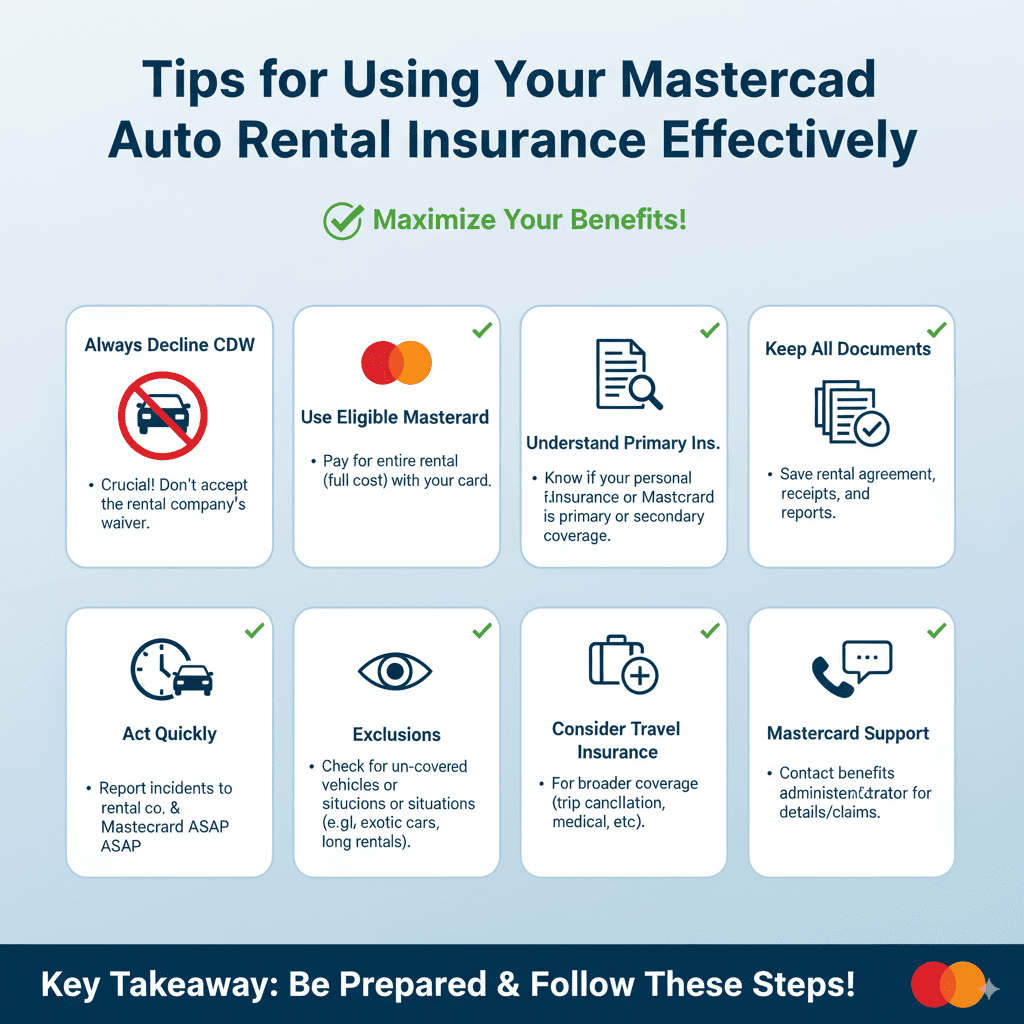

Tips for Using Your Mastercard Auto Rental Insurance Effectively

To make the most of your Mastercard’s car rental insurance and ensure a smooth experience, follow these tips:

- Always Declining the Rental Company’s CDW/LDW: This is the most critical step. If you accept the rental company’s waiver, you forfeit your credit card benefit for that rental.

- Use Your Mastercard for the Entire Rental: Pay for the full rental cost, including taxes and fees, with your eligible Mastercard. Don’t split payments unless absolutely unavoidable (and even then, check the terms).

- Understand Your Primary Insurance: Know if your personal auto insurance or another credit card covers rental cars. If your Mastercard benefit is secondary, your other insurance will be the first line of defense.

- Keep All Rental Documents: The rental agreement, damage reports, receipts, and any communication with the rental company are vital for claims.

- Act Quickly After an Incident: If the car is damaged or stolen, report it to the rental company immediately. Then, contact the Mastercard benefits administrator as soon as possible to initiate your claim.

- Review Exclusions Carefully: Be mindful of what types of vehicles or rental situations are not covered to avoid surprises.

- Consider Travel Insurance for Broader Coverage: If you need more comprehensive coverage, such as trip cancellation, lost luggage, or medical emergencies, consider purchasing a separate travel insurance policy.

External Resources for Authoritative Information

For official details and to dive deeper into specific terms and conditions, it’s always best to consult the card issuer directly or refer to authoritative resources. While benefits can change, here are some general navigational points:

Your specific credit card issuer (e.g., Chase, Citi, Capital One, Bank of America) will have the most accurate policy details for the Mastercard products they offer. You can find this information on their respective financial institution websites. For instance, looking up the benefits guide for your specific card account is the best first step. Reputable financial advice sites often compile comparisons of credit card benefits, but always cross-reference with your direct issuer’s documentation.

Frequently Asked Questions (FAQ)

Q1: Do all Mastercard cards include car rental insurance?

A1: No, not all Mastercard cards offer this benefit. It is typically found on premium card tiers like World Mastercard and World Elite Mastercard. You should always verify the specific benefits of your card.

Q2: What is the difference between primary and secondary car rental insurance?

A2: Primary insurance covers rental car damage before any other insurance you may have. Secondary insurance only covers costs after your primary insurance (like your personal auto policy) has paid its limits. Mastercard benefits are often secondary.

Q3: If my Mastercard covers rental cars, do I still need to buy insurance from the rental company?

A3: To use your Mastercard benefit, you must decline the rental company’s Collision Damage Waiver (CDW) or Loss Damage Waiver (LDW). If you accept the rental company’s coverage, you forfeit your credit card’s protection for that rental.

Q4: What types of vehicles are typically NOT covered by Mastercard’s rental car insurance?

A4: Coverage usually excludes luxury cars, exotic vehicles, antique cars, larger trucks or vans (with more than a certain passenger capacity), RVs, and motorcycles. Always check your card’s specific terms.

Q5: How long is the rental period usually covered by my Mastercard’s benefit?

A5: Most Mastercard auto rental CDW/LDW benefits cover rentals up to a certain number of consecutive days, commonly 30 or 31 days. Longer rentals might not be fully covered.

Q6: What should I do if the rental car is damaged while I have my Mastercard’s insurance on it?

A6: First, report the damage to the rental car company immediately. Then, contact your credit card’s benefits administrator as soon as possible to start the claims process. Be prepared to provide all rental documentation.

Q7: Can I use my Mastercard’s rental car insurance if I’m renting a car overseas?

A7: Coverage for international rentals varies significantly. Some premium Mastercard cards offer international coverage, while others do not. It is crucial to check your specific card’s benefits guide or contact your issuer to confirm details for international rentals.

Conclusion: Smart Savings on Your Next Rental

Navigating the world of car rental insurance can seem complicated, but understanding your Mastercard benefits can make a big difference. By knowing when and how your card provides Auto Rental Collision Damage Waiver coverage, you can potentially save a significant amount of money on your next rental. Remember to always use your eligible Mastercard for the entire rental, decline the rental company’s pricey insurance, and be aware of your card’s specific terms, conditions, and exclusions. This vital guide should equip you with the knowledge to rent smarter and travel with confidence, knowing your Mastercard might just have your back.