How to Use CPN for CA: Essential Guide

CPN for CA: Use your Commercial Paper Number (CPN) to establish credit and secure loans or rentals when you don’t have a traditional credit history. It’s a smart way for new businesses or individuals to build financial credibility.

Car ownership is fantastic, but sometimes getting that first car, renting a reliable apartment, or even starting a business can feel like a roadblock. Many of us have tried to get a loan or rent a place only to be told, “Sorry, your credit history isn’t strong enough.” It’s frustrating, right? Especially when you have a solid income and just need a fair chance. Fortunately, there’s a clever tool called a Commercial Paper Number (CPN) that can help you build a financial identity even if you’re starting with a blank slate. This guide will walk you through exactly how to use your CPN for credit applications, making those big steps much smoother.

What is a CPN and Why is it Important for You?

A Commercial Paper Number, or CPN, is essentially an alternative nine-digit number that individuals can use to establish a credit profile separate from their Social Security Number (SSN). Think of it as a financial identifier that helps lenders and creditors see your creditworthiness without directly tying it to your personal SSN. This is super helpful if you’re new to credit, have a less-than-perfect credit history you want to move past, or if you’re starting a business and need a distinct financial identity.

Using a CPN can open doors that might otherwise stay shut. For example, imagine trying to get approved for a car loan or a new apartment lease. Lenders and landlords often check your credit history. If you don’t have much of a history, or it contains negative marks, you might be denied. A CPN can help create a fresh start, allowing you to build positive credit experiences from scratch.

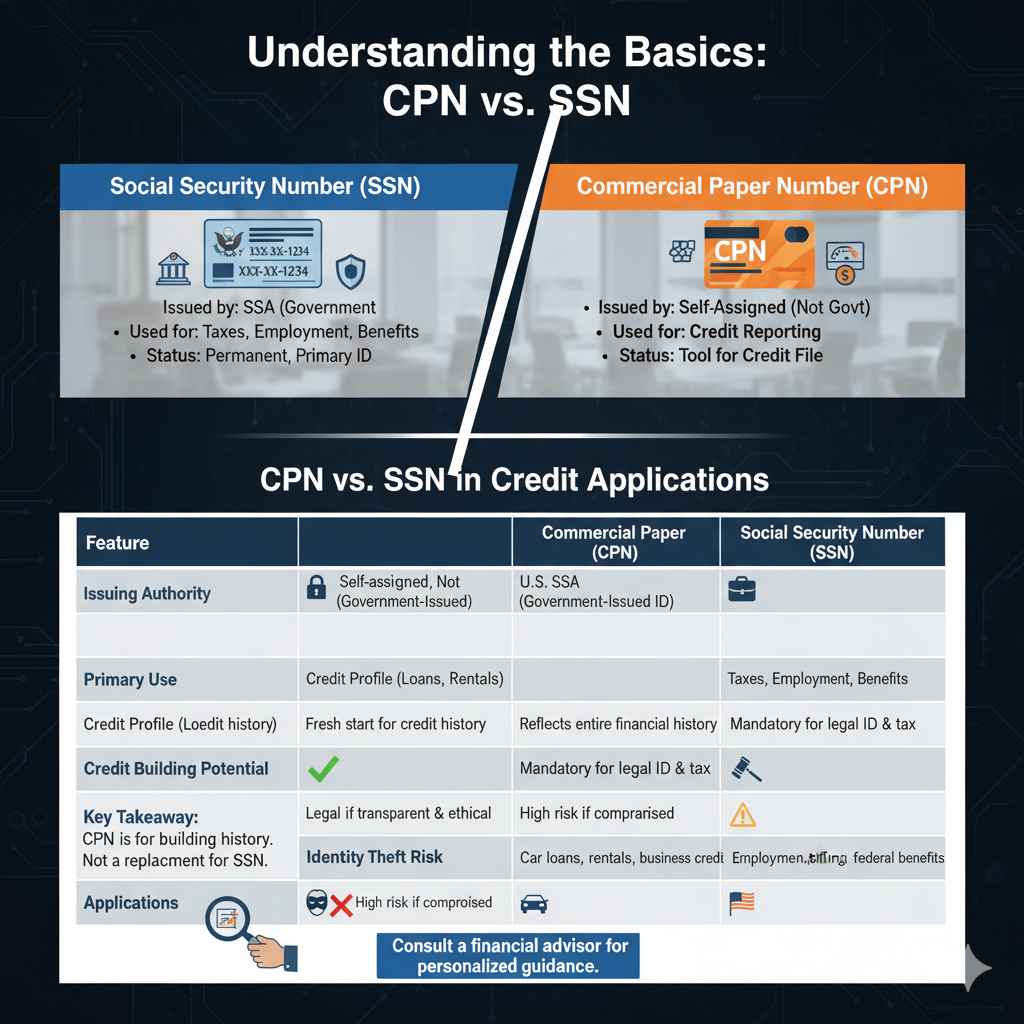

Understanding the Basics: CPN vs. SSN

It’s vital to understand the difference between a CPN and your Social Security Number (SSN). Your SSN is your primary identifier for government, tax, and employment purposes. It’s deeply connected to your entire financial and personal history with federal agencies. A CPN, on the other hand, is designed for credit reporting purposes. It’s not a replacement for your SSN for tax or employment situations, but rather a tool to build a credit file.

Here’s a simple breakdown:

- Social Security Number (SSN): Issued by the Social Security Administration (SSA). Used for taxes, employment, and government benefits. Your permanent, primary personal identifier.

- Commercial Paper Number (CPN): A self-assigned number used to establish a separate credit profile. Not officially issued by a government agency. Primarily for credit applications.

Using a CPN requires careful handling. It’s about building credit responsibly. The goal is to create a positive payment history associated with your CPN, which lenders can then use to make lending decisions, especially for things like auto loans or rental agreements. It’s not about hiding information, but about providing a clean slate for credit assessment.

Why Would Someone Use a CPN for Credit Applications?

There are several common reasons why people turn to using a CPN for credit applications, especially for significant purchases like a car or securing a place to live. Many individuals, particularly young adults just starting out or those who have faced financial difficulties, may have limited or damaged credit histories. Without a strong credit score, tasks like buying a car or renting an apartment can become incredibly challenging.

Here are some key scenarios where a CPN can be beneficial:

- Limited Credit History: If you’re new to the adult world or haven’t used credit much, you might not have a credit score that lenders recognize. A CPN helps you build this from the ground up.

- Damaged Credit History: Past financial mistakes, such as late payments or defaults, can weigh down your credit score. A CPN allows you to start fresh without those past issues affecting new credit applications.

- Privacy Concerns: Some individuals prefer to keep their personal SSN separate from credit applications to minimize potential identity theft risks.

- Business Credit Building: Entrepreneurs may use a CPN to establish credit for their business entities, keeping business finances distinct from personal finances.

It’s important to approach CPNs with transparency and legality in mind. The goal is to build credit ethically. Think of it as creating a new financial identity for credit purposes, allowing you to prove your ability to handle financial obligations responsibly. This can be a game-changer for achieving major life goals like owning a car or securing stable housing.

Step-by-Step Guide: How to Use CPN for CA (Car Applications)

Using a CPN for a car application involves a series of deliberate steps to ensure you’re building credit correctly and ethically. It’s not as complicated as it might sound, and with a bit of patience, you can establish a solid credit foundation. Remember, the primary goal is to build a positive payment history associated with your CPN.

1. Obtain Your Credit Profile Numbers

Before you can use a CPN, you need to establish the necessary credit reporting accounts linked to it. This usually involves obtaining specialized credit accounts that report to major credit bureaus. These accounts are often offered by specific financial institutions and may require a small deposit or fee to set up. It’s crucial to ensure these are legitimate credit-building accounts that will report your payment history.

You’ll typically need to establish primary accounts that report to all three major credit bureaus: Experian, Equifax, and TransUnion. This often includes things like:

- A Secured Credit Card: This is a credit card secured by a cash deposit you make. It’s an excellent way to start building credit responsibly.

- An Experian Boost™ account: While not a traditional CPN account, services that help build credit profiles are available.

- Other specialized credit services that explicitly state they report to all three major bureaus.

The key here is to ensure these accounts are being reported to the credit bureaus under your CPN, not your SSN. Always verify with the provider that they report to all three bureaus (Experian, Equifax, TransUnion).

2. Build Positive Payment History

Once you have your accounts set up using your CPN, the next crucial step is to use them responsibly and build a positive payment history. This means making all your payments on time, every time.

- Pay Your Bills On Time: Whether it’s your secured credit card or any other account reporting to your CPN, always make at least the minimum payment by the due date. Ideally, pay the full balance to avoid interest charges.

- Keep Credit Utilization Low: For credit cards, try to keep your balance well below your credit limit. A utilization ratio of 30% or less is generally recommended. For example, on a $1,000 credit limit, try to keep your balance below $300.

- Avoid Opening Too Many Accounts at Once: While it might be tempting to open multiple accounts to build credit faster, opening too many in a short period can negatively impact your credit score by making you appear risky.

Consistency is key. It takes time for positive actions to reflect on your credit report and build a strong profile. Be patient, and focus on developing good financial habits.

3. Obtain Your Credit Reports

After a few months of consistent, on-time payments, it’s time to check your progress. You’ll want to obtain copies of your credit reports from each of the three major bureaus: Experian, Equifax, and TransUnion.

You can get your free credit reports annually from each bureau at AnnualCreditReport.com. This is a service mandated by federal law, so it’s a reliable and free way to see your credit history.

When you review your reports, look for:

- That your accounts are listed correctly under your CPN.

- That your payment history is reported accurately (e.g., no late payments).

- That there are no errors or fraudulent accounts.

If you find any mistakes, report them immediately to the credit bureau. Correcting errors is an important part of maintaining a clean credit file. A strong, accurate credit report is your best asset when applying for a car loan.

4. Prepare for the Car Application

Once you have a solid credit history built under your CPN and verified through your credit reports, you’re ready to apply for a car loan. Many dealerships and lenders understand the concept of alternative credit building and may be open to working with you.

Here’s what to expect and prepare for:

- Be Honest and Transparent: When filling out loan applications, you may encounter fields for your SSN. Understand the specific lender’s policy for CPNs. Some lenders have specific procedures for CPNs, while others may not be equipped to handle them. Always follow the lender’s instructions.

- Gather Supporting Documents: Besides your CPN credit reports, lenders will likely ask for proof of income, such as pay stubs, bank statements, or tax returns, to show you can afford the monthly payments.

- Shop Around for Lenders: Don’t settle for the first offer. Compare interest rates, loan terms, and monthly payments from different lenders. This can include traditional banks, credit unions, and dealerships’ finance departments. Some lenders are more CPN-friendly than others.

- Understand the Terms: Before signing anything, read the entire loan agreement carefully. Know the interest rate (APR), loan term (how many months you’ll pay), and any fees involved.

Applying for a car loan with a CPN is about presenting yourself as a reliable borrower. By demonstrating a history of responsible credit management, you increase your chances of approval and securing favorable loan terms.

CPN for Other Credit Applications (Rentals, Loans & More)

The principles of using a CPN extend beyond just car applications. It’s a versatile tool for building financial credibility in various aspects of your life. Whether you’re looking to rent an apartment, secure a personal loan, or even get utilities, a well-established CPN can be your ally.

Using a CPN for Rental Applications

Landlords often check credit reports to gauge a tenant’s reliability and ability to pay rent on time. If your credit history is thin or contains negative remarks under your SSN, a CPN can provide a clean slate.

When applying for a rental, you’ll typically need to:

- Present your CPN credit report: Show potential landlords evidence of your responsible financial behavior.

- Have established accounts: Similar to car loans, having utility accounts, secured credit cards, or other tradelines reported to your CPN demonstrates consistent payment habits.

- Provide proof of income: As always, landlords need to see you can afford the rent.

- Consider a larger security deposit: In some cases, offering a slightly larger security deposit in exchange for a rental agreement might be an option, especially if your credit profile is still new.

Using a CPN Untuk Personal Loans

Securing a personal loan can be challenging without a strong credit history. A CPN allows you to build a credit file that lenders can assess.

Follow the same steps: establish credit-building accounts, make on-time payments, and periodically check your credit reports. When applying for personal loans, lenders look for a history of responsible borrowing and repayment. A CPN can help you present this positive track record.

Using a CPN for Business Credit

For entrepreneurs, establishing business credit separate from personal credit is crucial. A CPN can be a valuable tool in this process.

Here’s how it can help:

- Separate Personal and Business Finances: Using a CPN for business credit applications helps keep your business’s financial identity distinct from your personal one.

- Access Business Loans and Lines of Credit: Lenders for business funding often require a credit history. A CPN can help you start building this.

- Get Better Terms on Business Purchases: Building business credit can lead to better terms with suppliers and vendors.

It’s important to distinguish between using a CPN for personal credit building and business credit building. While the principles are similar (establishing accounts, making payments), the specific accounts and lenders you work with might differ.

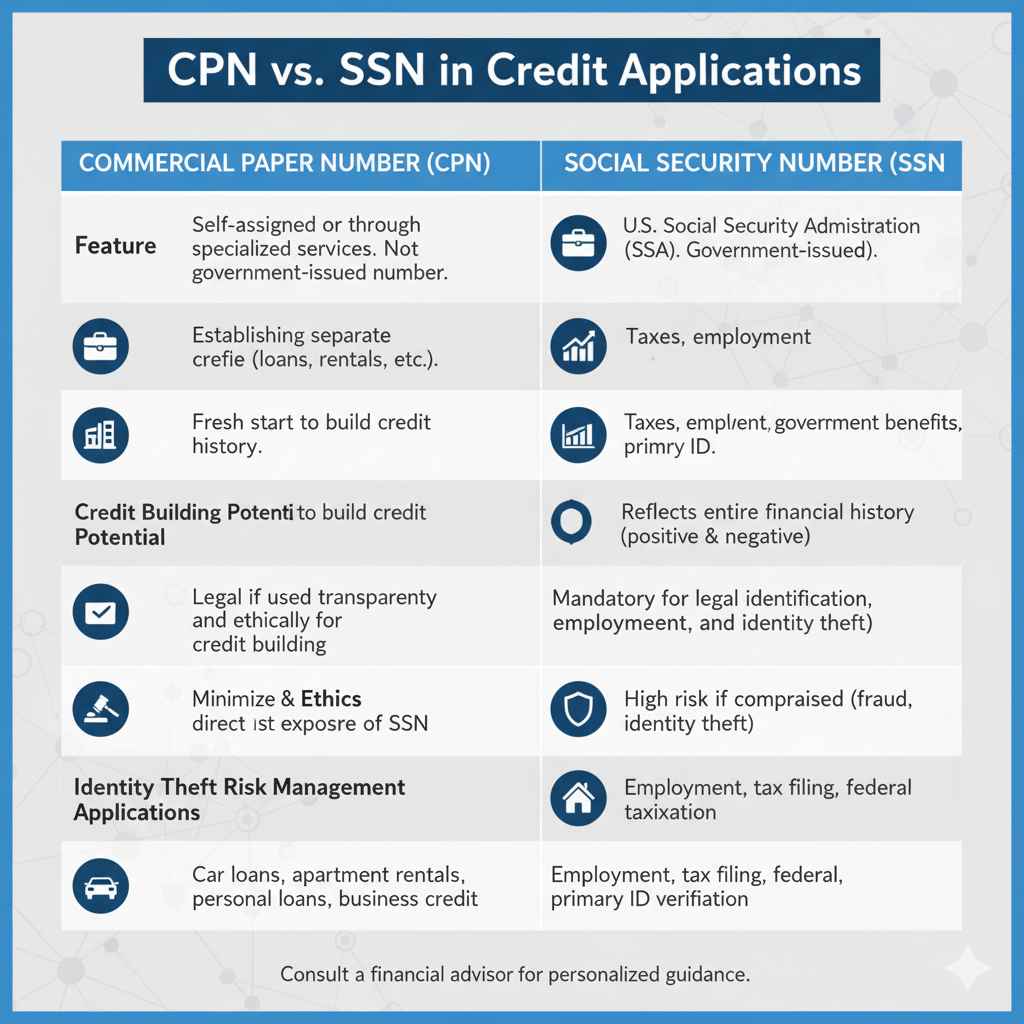

Table: CPN vs. SSN in Credit Applications

To further clarify the role of each number, here’s a comparison table:

| Feature | Commercial Paper Number (CPN) | Social Security Number (SSN) |

|---|---|---|

| Issuing Authority | Self-assigned or through specialized services. Not a government-issued number. | U.S. Social Security Administration (SSA). A government-issued identification number. |

| Primary Use | Establishing a separate credit profile for credit applications (loans, rentals, etc.). | Taxes, employment, government benefits, primary personal identification. |

| Credit Building Potential | Allows for a fresh start to build credit history. | Reflects your entire financial history, both positive and negative. |

| Legality & Ethics | Legal if used transparently and ethically for credit building. Must align with lender policies. | Mandatory for legal identification, employment, and taxation. |

| Identity Theft Risk Management | Can help minimize direct exposure of SSN on credit applications. | If compromised, can lead to significant identity theft and financial fraud. |

| Applications | Car loans, apartment rentals, personal loans, business credit. | Employment, tax filing, federal benefits, primary identification verification. |

Potential Challenges and What to Watch Out For

While a CPN can be a powerful tool, it’s not without its challenges, and it’s crucial to be aware of potential pitfalls. Responsible use and understanding the landscape are key to avoiding issues.

Legality and Ethical Considerations

It’s imperative to use a CPN legally and ethically. A CPN is a tool for building credit, not for defrauding lenders or hiding from genuine financial obligations. Lenders and creditors have the right to ask for your SSN for identity verification purposes, especially for official government-related matters or when required by law. Misrepresenting yourself or using a CPN to deceive can lead to serious legal consequences, including denial of credit, account closure, and even legal prosecution. Always ensure you are following the guidelines set by financial institutions and relevant laws. You can learn more about credit reporting from the Consumer Financial Protection Bureau (CFPB).

Lender and Creditor Acceptance

Not all lenders or creditors are familiar with or willing to accept CPNs. Some may insist on using your SSN for all credit applications. This is often because their systems are built around SSNs, or they have strict policies regarding identity verification. It’s important to research potential lenders and landlords in advance to see if they have experience or a policy for accepting CPNs. If they don’t, you may need to build credit using your SSN or find alternative options.

Building a Solid Credit File Takes Time

Establishing a strong credit history with a CPN, just like with an SSN, requires patience and consistent responsible behavior. It doesn’t happen overnight. It typically takes several months to a year or more of on-time payments and positive credit management for a CPN-based credit file to become robust enough for lenders to rely on for significant applications like car loans.

Avoiding Scams

The CPN market can attract scammers. Be wary of services that promise guaranteed credit approval or claim to offer unique, government-issued CPNs. Legitimate CPNs are not officially issued by any government agency. If a service seems too good to be true, it likely is. Stick to reputable credit-building services and understand how the process works before paying any fees.

Frequently Asked Questions (FAQ)

What’s the fastest way to build credit with a CPN?

The fastest way to build credit with a CPN is to establish a few credit-building accounts (like secured credit cards or tradelines that report to all three bureaus) and use them consistently by making all payments on time and keeping balances low. Checking your credit reports regularly to ensure accuracy is also key.

Can I use a CPN for my primary identification?

No, your CPN is for credit building purposes only. Your Social Security Number (SSN) is your primary identification for government, employment, and tax purposes. You cannot use a CPN for these official functions.