What Does Charge Off Mean On A Car Loan: Essential Guide

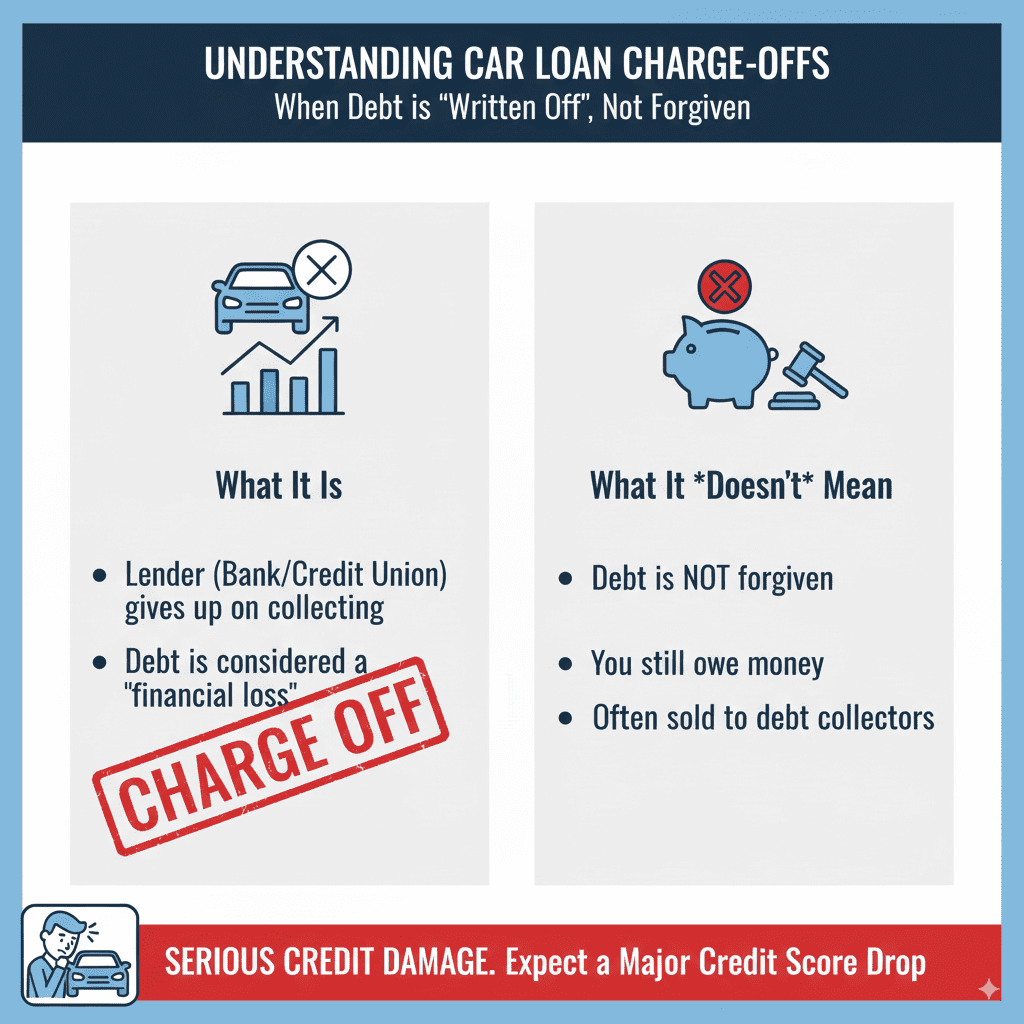

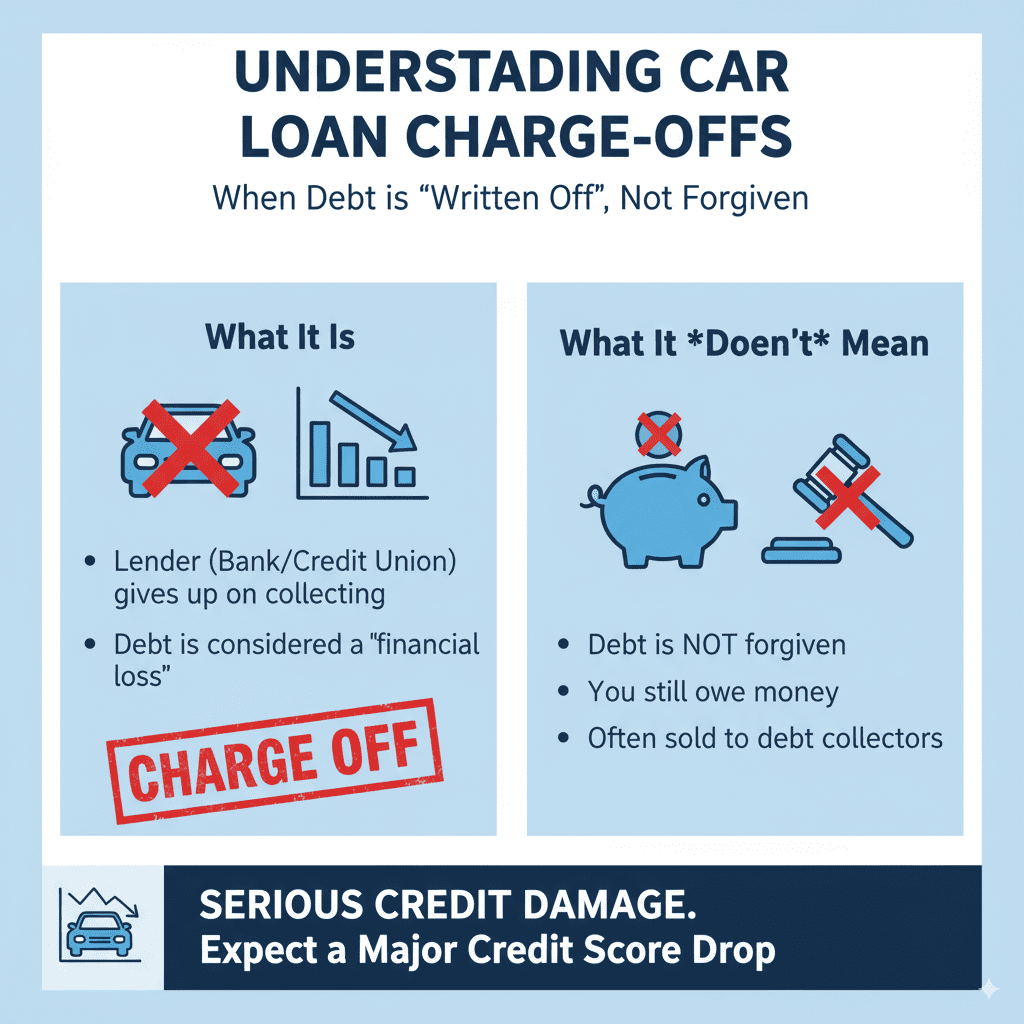

A car loan charge-off means the lender has given up trying to collect the debt. They write it off as a loss, but you still owe the money, and it severely damages your credit. It can lead to vehicle repossession and legal action.

Owning a car is exciting, but sometimes life throws curveballs, and making loan payments becomes tough. If you’ve missed payments, you might have come across scary terms like “charge-off.” It sounds serious, and it is, but understanding it is the first step to tackling it. Think of this guide as your friendly mechanic for financial terms – we’ll break down exactly what a car loan charge-off means, why it happens, and what you can do about it, all in simple terms. No confusing jargon, just clear, practical advice to help you navigate this tricky situation and get back on the road to financial wellness. Let’s dive in and make sense of it together!

Understanding What a Car Loan Charge-Off Really is

So, you’ve heard the term “charge-off” related to your car loan, and it sounds a bit alarming. Let’s break it down simply. When a lender, like your bank or credit union, says your car loan has been “charged off,” it’s their way of saying they’ve decided they probably won’t be able to collect the money you owe them. They’ve essentially written off this debt as a financial loss on their books.

This doesn’t mean you’re suddenly free from the debt! Far from it. It’s a serious step in the debt collection process. While the lender stops actively trying to collect from you directly in the traditional sense, they haven’t forgiven the debt. It’s more like they’re closing that chapter internally for accounting purposes and may pass the debt on to other agencies.

When Does a Car Loan Get Charged Off?

Lenders don’t just wake up one day and decide to charge off a loan. There’s a process, and it usually involves a significant period of missed payments. Typically, a car loan is considered for charge-off after you’ve been delinquent for a certain amount of time, often around 120 days (about four months) of missed payments. However, this timeframe can vary depending on the lender’s policies and the specific terms of your loan agreement.

The lender usually tries various methods to get you to pay before reaching this point. This can include:

Sending reminder notices and emails.

Making phone calls to discuss payment options.

Possibly offering a payment plan or deferment.

If all attempts to recover the money fail through these usual channels, they will then proceed with the charge-off.

The Immediate Impact of a Charge-Off

The moment your car loan goes into charge-off status, several things happen, and they’re not pleasant. You need to be prepared for the consequences.

1. Severe Credit Score Damage: This is the most significant and immediate impact. A charge-off is a major red flag to future lenders and credit reporting agencies. It signals that you failed to meet your financial obligations. This will drastically lower your credit score, making it very difficult to get approved for new loans, credit cards, or even rent an apartment in the future. According to Experian, a credit reporting agency, the average credit score for someone with a charged-off account can drop significantly, often by over 100 points.

2. Vehicle Repossession: If you haven’t already had your car repossessed, a charge-off often makes it a certainty. Lenders want to recoup some of their losses, and the car itself is their collateral. Once charged off, they are highly likely to take steps to repossess the vehicle. They can do this without prior notice in many states, though laws vary.

3. Collection Efforts Change: While the original lender might stop direct collection, they often sell the debt to a third-party debt collection agency. These agencies can be very persistent and may use various tactics to try and get you to pay the balance.

4. Potential for Lawsuits and Wage Garnishment: The debt doesn’t disappear. If the lender or collection agency can’t recover the amount owed through repossession or collections, they might pursue legal action. This could lead to a court judgment against you, which can result in wage garnishment (having a portion of your paycheck automatically sent to the creditor) or liens on other assets.

What Happens to Your Car After a Charge-Off?

The most visible consequence of a car loan charge-off is what happens to your vehicle. Since the car serves as collateral for the loan, the lender has a right to take it back if you don’t make your payments.

Vehicle Repossession

When a car loan is charged off, especially if the car is still in your possession, repossession is a very common next step.

The Lender Takes the Car: The lender (or an agent they hire) will locate your vehicle and take it back. In most places, they don’t need a court order to do this, and they can repossess it even if it’s parked in your driveway or on the street. It’s important to know your state’s specific laws regarding repossession, as some offer limited protections.

Sale of the Vehicle: After repossessing the car, the lender will typically sell it to try and recover some of the money you owe. This sale is often done at an auction.

Deficiency Balance: Here’s a crucial point: the sale of your car might not cover the full amount you owe on the loan. The difference between the sale price of the car and the outstanding loan balance (plus any fees for towing, storage, and the sale itself) is called the “deficiency balance.” You are still legally responsible for this remaining amount.

Dealing with the Deficiency Balance

That deficiency balance is a significant part of understanding what a charge-off means. Even after losing your car, you still owe the money.

Notice of Sale: In many states, the lender is required to provide you with notice of the intent to sell the vehicle and information about where and when the sale will occur. This gives you a chance to potentially buy the car back or make arrangements.

Your Obligation Remains: If the sale doesn’t cover the debt, you’ll receive a bill or a notice for the deficiency. This amount will likely be sent to a collection agency, and as mentioned, it can lead to further legal action.

It’s a tough situation to lose your car and still owe money, but understanding this process helps you prepare and know what to expect.

Can You Prevent a Car Loan Charge-Off?

The best way to deal with a charge-off is to prevent it from happening in the first place. If you’re struggling to make payments, acting quickly is key.

Communicate with Your Lender Immediately

If you anticipate difficulty making your car payments, don’t wait until you’ve missed several. Reach out to your lender before you miss a payment.

Be Honest: Explain your situation clearly and honestly. Lenders are more likely to work with you if you’re proactive.

Explore Options: Ask about potential solutions such as:

Forbearance: This is a temporary period where you can pause or reduce your payments. The missed payments are usually added to the end of the loan term or spread out over future payments.

Payment Plan: A lender might allow you to catch up on missed payments by spreading them over a few months, in addition to your regular monthly payment.

Loan Modification: In some cases, the lender might agree to change the terms of your loan, such as extending the loan term to reduce monthly payments, or even lowering the interest rate. This is less common but possible.

Financial Assistance and Budgeting

Sometimes, the issue is a temporary cash flow problem, while other times it’s a more significant budgeting challenge.

Review Your Budget: Understand where your money is going. Look for areas where you can cut back on expenses to free up money for your car payment. The Consumer Financial Protection Bureau (CFPB) offers excellent tools and advice for creating and managing a budget.

Seek External Help: If you’re overwhelmed, consider talking to a non-profit credit counseling agency such as those accredited by the Institute of Credit Management, which can help you create a debt management plan.

What to Do If Your Car Loan Has Been Charged Off

If you’re already facing a charge-off, don’t despair. While it’s a serious financial setback, there are steps you can take.

1. Understand the Next Steps for Collection

When a debt is charged off, the original lender usually either tries to collect it themselves or sells it to a debt collection agency. This is a critical phase to be aware of.

Debt Collector Contact: You’ll likely be contacted by a debt collector. They will try to negotiate a payment.

Know Your Rights: Debt collectors are regulated by the Fair Debt Collection Practices Act (FDCPA) in the United States. This law protects you from harassment and abusive practices. You have rights, such as the right to request validation of the debt and to have them stop contacting you if you send them a written request. You can learn more about your rights on the Federal Trade Commission (FTC) website.

2. Negotiate a Settlement

Even though you owe the full amount, you might be able to negotiate a settlement with the debt collector for a lesser amount.

Lump-Sum Payment: Collectors often buy debt for pennies on the dollar. They’re often willing to accept a one-time lump-sum payment that is less than the full balance owed to close the account.

Payment Plans: If you can’t afford a lump sum, you might be able to negotiate a payment plan. Be realistic about what you can afford.

Get It in Writing: Always get any settlement agreement or payment plan in writing before you make any payment. This protects you and ensures the terms are clear.

3. Rebuilding Your Credit

A charge-off will stay on your credit report for seven years. During this time, your priority should be rebuilding your credit.

Pay Bills On Time: The most important factor for your credit score is timely payment. Ensure all your current bills are paid on time.

Secured Credit Cards: Consider applying for a secured credit card. You make a deposit, which becomes your credit limit. Use it for small purchases and pay it off in full each month. This helps build positive credit history.

Credit-Builder Loans: Some banks and credit unions offer credit-builder loans, which are small loans where the money is held in an account and released to you after you’ve paid it off.

Monitor Your Credit Report: Regularly check your credit report from all three major bureaus (Equifax, Experian, and TransUnion) to ensure accuracy and track your progress. You can get a free copy of your credit report annually from each bureau at AnnualCreditReport.com.

Impact on Your Credit Report: A Deeper Look

Let’s talk more about how a charge-off affects your credit report. This is probably the most long-lasting consequence, so it’s vital to understand.

What Does it Look Like on Your Report?

When a car loan is charged off, it’s clearly marked on your credit report. You’ll typically see codes indicating the account status, such as “Charged Off” or “CO.” It will also show the date of the charge-off and the amount of the debt.

| Credit Report Item | Impact of Charge-Off | Duration |

|---|---|---|

| Credit Score | Significant decrease (often 100+ points) | Carries forward until removed |

| Payment History | Negative remarks from missed payments preceding charge-off | 7 years from original delinquency date |

| Overall Account Status | Marked as “Charged Off” | 7 years from original delinquency date |

| Collection Accounts | If sold to collectors, a new collection entry appears | 7 years from original delinquency date |

How Long Does a Charge-Off Stay on Your Credit Report?

In most cases, a charge-off will remain on your credit report for seven years from the date of the original delinquency that led to the charge-off. For example, if you stopped paying in January 2023 and the loan was charged off in April 2023, it will likely fall off your report in January 2030 (seven years from the first missed payment).

The Clock Starts Early: It’s important to note that the seven-year clock usually starts from the date of the first missed payment that led to the charge-off, not the date the lender officially charged it off.

After Seven Years: Once a charge-off falls off your credit report, it can no longer negatively impact your credit score. However, it’s important to know that if a collection agency sued you and obtained a court judgment, that judgment can remain on your credit report for even longer, sometimes up to 10 years or more, depending on state laws.

Can You Remove a Charge-Off Early?

Generally, no. You cannot force a lender or collection agency to remove an accurate charge-off from your credit report before the seven-year mark.

However, there are a few exceptions:

Errors: If there are inaccuracies in the reporting of the charge-off (e.g., wrong date, wrong amount, or it’s not your debt), you can dispute it with the credit bureaus. This is why checking your reports is so important. You can initiate a dispute through the IdentityTheft.gov portal or directly with the credit bureaus.

Settlement and Deletion: In some rare cases, you might be able to negotiate with a debt collector to have the charge-off removed from your credit report as part of a settlement agreement. This is often called a “pay for delete” agreement. However, many collectors will not agree to this. It’s worth asking, but don’t count on it.

The Difference: Charge-Off vs. Repossession vs. Foreclosure

It’s easy to get these terms mixed up, as they can all relate to losing a financed asset. Let’s clarify the distinctions:

Charge-Off

What it is: The lender declares the debt unlikely to be collected and writes it off as a financial loss.

Asset Involved: Can apply to any type of loan or debt (car loan, credit card, personal loan).

Impact: Severe credit score damage, continued obligation to pay, potential repossession or legal action.

Repossession

What it is: The lender legally takes back a financed asset (like a car) because the borrower has failed to make payments.

Asset Involved: Primarily applies to assets used as collateral for a loan (cars, boats, RVs).

Impact: Loss of the asset, often results in a deficiency balance, significant credit score damage.

Foreclosure

What it is: The legal process where a lender takes ownership of a property (like a house) when the borrower defaults on the mortgage payments.

Asset Involved: Specifically applies to real estate (homes, land).

Impact: Loss of home, potential deficiency judgment, severe credit score damage.

Think of it this way: A charge-off is an accounting term for the lender about bad debt. Repossession is the action of taking back collateral (like a car) when a loan for that collateral is in default. Foreclosure is the specific legal process for taking back real estate collateral. A car loan charge-off very often leads to* repossession.

Frequently Asked Questions (FAQ)

Q1: What does “charge off” mean for my car loan?

A1: A car loan charge-off means the lender has given up on trying to collect the debt from you and has written it off as a loss on their books. You still owe the money, though, and it will severely damage your credit score.

Q2: Will I lose my car if my loan is charged off?

A2: It’s very likely. Lenders usually repossess collateral, like your car, after a charge-off to try and recover some of the money owed.

Q3: Does a charge-off mean the debt is forgiven?

A3: No, absolutely not. The debt is not forgiven. The lender has just changed how they account for it internally. You are still legally obligated to pay it, and it can be sold to a collection agency.

Q4: How long does a charge-off stay on my credit report?

A4: A charge-off typically stays on your credit report for seven years from the date of the original delinquency that led to the charge-off.