Can I Sell My Car With Open Claim? Essential Guide

Yes, you can often sell your car with an open insurance claim, but it requires careful handling of the situation. Transparency with potential buyers and understanding how the claim process works with ownership transfer are key. This guide will walk you through everything you need to know to navigate this common scenario smoothly.

Selling your car can be a big decision, and things can get a bit confusing when you have an open insurance claim related to it. You might be wondering, “Can I even do this?” or “How does selling my car affect my claim, and vice versa?” It’s a common question, and it’s totally understandable to feel a little uncertain. The good news is, it’s often possible to sell your car even with an active claim. Think of this guide as your friendly roadmap, breaking down all the steps and important points so you can sell with confidence and clarity. We’ll help you understand the process, what disclosures you need to make, and how to handle the paperwork smoothly.

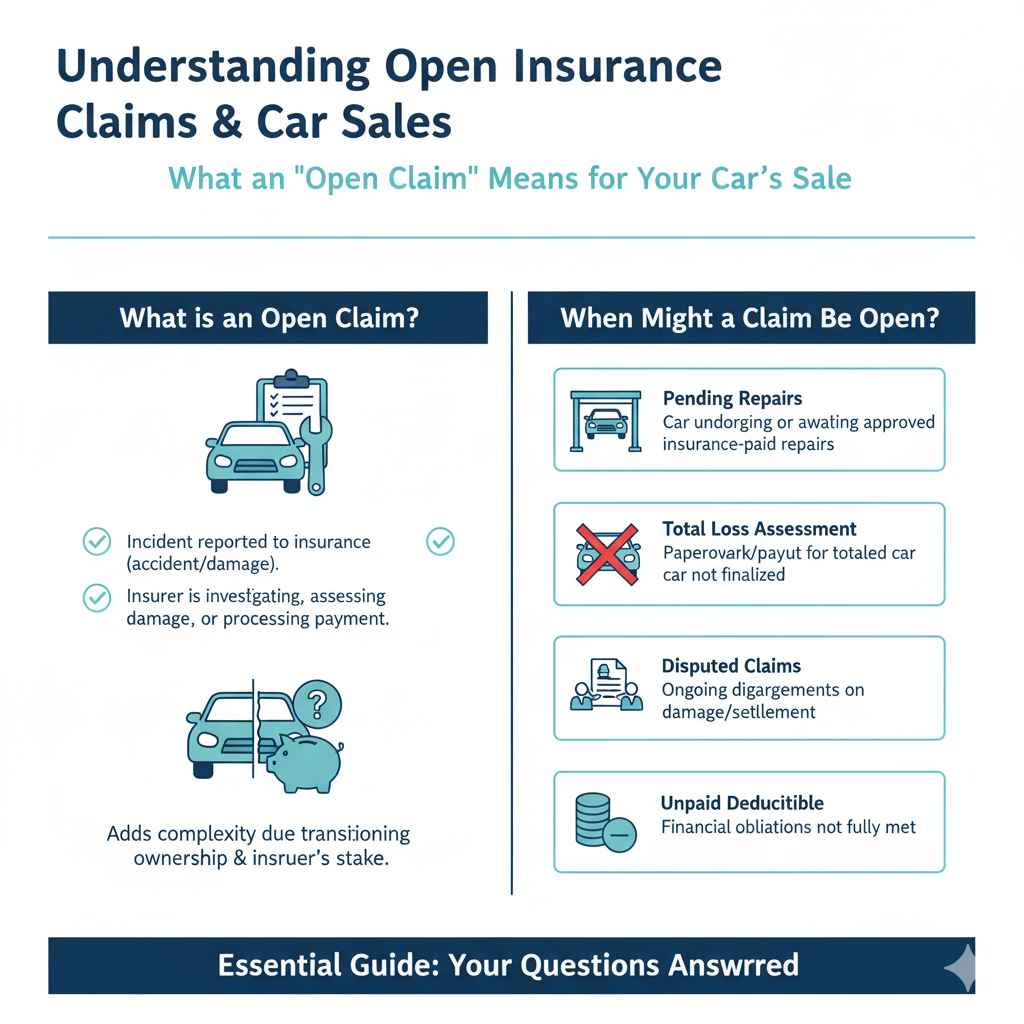

Understanding Open Insurance Claims and Car Sales

An “open insurance claim” means you’ve reported an incident (like an accident or damage) to your insurance company, and they are in the process of investigating, assessing the damage, or processing a payment. This could be a claim where your car is being repaired, or one where you’re waiting for a settlement amount because the car is a total loss.

Selling a car while a claim is open adds a layer of complexity. The core issue is that ownership of the car might be in transition while the insurance company still has a stake in the outcome of the claim. This is especially true if the insurance company has paid out a significant amount towards repairs or if they have declared the car a total loss and you’re awaiting their final settlement check.

When Might You Have an Open Claim?

- Pending Repairs: Your car was damaged in an incident, and it’s currently undergoing repairs paid for by insurance, or the repairs are approved but not yet completed.

- Total Loss Assessment: The insurance company has assessed the damage and determined the cost to repair exceeds a certain percentage of the car’s value. They may have offered you a settlement, but the paperwork or payout hasn’t been finalized.

- Disputed Claims: There might be ongoing discussions or disputes with the insurance company regarding the extent of damage or the fair settlement amount.

- Unpaid Deductible: Even if repairs are done, if your deductible hasn’t been fully paid, the claim technically might still be considered open by some insurers until all financial obligations are met.

The Impact of an Open Claim on Your Sale

The existence of an open claim can affect your car sale in several ways:

- Transparency is Crucial: You must disclose the open claim to any potential buyer. Hiding this information can lead to legal trouble and severe trust issues.

- Repair Status Matters: If your car is still being repaired, the sale might need to be contingent on the completion of those repairs. If it’s a total loss, the process often involves the insurance company and the buyer.

- Ownership and Payouts: If the car is a total loss and the insurance company has issued a payout, they might have a lien on the title until they receive the damaged vehicle or the full settlement amount. This means the payout technically belongs to the insurer if they’ve paid you for the car’s value.

- Resale Value: A car that has been involved in a significant accident, even if repaired, might have a lower resale value. An open claim adds another layer of uncertainty for buyers.

Scenario 1: Selling a Car That’s Being Repaired

If your car had minor to moderate damage and is currently in a body shop or waiting for repairs, selling it can be managed, but it requires careful coordination.

Steps to Take:

- Communicate with Your Insurer: Inform your insurance adjuster that you intend to sell the vehicle. Ask them how they want to proceed with the repairs. They might want to pause repairs, complete them, or adjust their involvement based on your sale plans.

- Get a Repair Estimate: If repairs aren’t started, get a clear estimate of the cost and time needed. This helps you and potential buyers understand what’s involved.

- Inform Potential Buyers: Be upfront about the damage and the ongoing claim. Explain that the car is being repaired under an insurance claim.

-

Decide on Repair Completion:

- Option A: Sell As-Is (Without Repairs): You can sell the car in its current state. The buyer would then be responsible for completing the repairs, potentially using the insurance payout if that’s part of the agreement. This usually means a lower sale price.

- Option B: Complete Repairs Before Selling: You can wait for your insurance company to complete the repairs. Once done, you can sell the car as a repaired vehicle. This might fetch a better price but delays your sale.

- Transfer of Ownership: Once a sale is agreed upon, ensure all paperwork reflects the status of the repairs and the claim. If the insurance company paid for repairs directly to the shop, and you are selling immediately after, the title should be clear of any liens. If they issued you a check, and you haven’t paid the shop or surrendered the damaged vehicle (in case of total loss), the situation is more complex as discussed below.

Scenario 2: Selling a Car Declared a “Total Loss”

This is where the process gets more intricate. When a car is declared a “total loss,” it means the cost to repair it is more than its actual cash value (ACV) or a statutory limit set by the state. Your insurance company typically pays you the ACV and takes possession of the damaged vehicle. The car will then usually be sold for salvage.

If You Haven’t Received the Settlement:

If the insurance company hasn’t yet finalized the payout and taken possession of the car, you technically still own it. However, you cannot sell it to a third party without the insurance company’s agreement, as they have a vested interest in the salvage value.

If You Have Received the Settlement Check:

This is the most crucial scenario. When an insurance company declares a car a total loss and offers you a settlement, they are paying you the pre-accident value of your car. In exchange for this payment, they usually take ownership of the damaged vehicle. If you have accepted the settlement and received payment:

- The Insurance Company Owns the Car: Legally, the damaged car now belongs to the insurance company. They will arrange for it to be towed to a salvage yard.

- You Cannot Sell It: You cannot sell a car that you no longer own. Attempting to do so would be fraudulent.

- Lien on the Title: In some cases, especially if you have a loan on the car, the insurance company might pay off the loan directly and send you the remaining difference. They will then take the car. If they send you a check that includes the loan payoff, and you decide not to let them have the car and instead want to keep it (for its salvage value), you’ll need to discuss this with them. They will then deduct the salvage value from your settlement.

Important Note: If you have a loan on your vehicle, the insurance company will pay the loan balance directly to your lender before they would pay you the remaining amount. If the settlement amount is less than the loan balance, you will owe the lender the difference. This is a common point of confusion, so always clarify this with your insurer.

Selling a Car the Insurer Paid You For (and you kept the salvage)

If your insurer declared your car a total loss, paid you its ACV minus the salvage value, and you kept the damaged car, be aware of the following:

- Salvage Title: The vehicle’s title will be branded as “salvage.” This means it has been declared a total loss by an insurer and can only be legally driven after it has been repaired and passed a specific salvage inspection.

- Selling a Salvage Title Car: You can sell a car with a salvage title, but you must be completely upfront about its condition and the title status. Buyers are typically looking for projects or parts. The sale price will be significantly lower.

- Transparency is Paramount: Never hide the fact that the car has a salvage title. Honesty is your best policy to avoid legal repercussions and maintain your integrity.

Key Considerations for a Smooth Sale

Regardless of whether your car is being repaired or has been declared a total loss, here are some key points to keep in mind for a smoother selling process:

1. Full Disclosure and Honesty

As Md Meraj, your trusted automotive guide, I’ll stress this point repeatedly: honesty is always the best policy. Any potential buyer has the right to know the full history of the vehicle, including any open insurance claims, accidents, or if it has been declared a total loss.

- When to Disclose: Disclose the claim status early in the conversation, ideally before any serious buyer engagement or test drives.

- What to Disclose: Explain the nature of the claim (e.g., collision, vandalism), the current status (repairs ongoing, awaiting assessment, total loss), and what the next steps might be.

- Consequences of Non-Disclosure: Failing to disclose can lead to legal disputes, the buyer backing out, or even lawsuits for misrepresentation.

2. Understanding Your Insurance Policy

Your insurance policy documents are your best friend here. Read them carefully or contact your insurer to understand the specifics of claims involving total losses and ownership transfer. Some policies might have clauses about selling a vehicle with an open claim.

3. The Role of the Title

The car’s title is a legal document that proves ownership. If your car is a total loss and the insurance company has paid you its value, they essentially become the owner of the salvage. You will need to surrender the title to them. If you keep the salvage, the title will be branded as “salvage.” A clear title is always preferred by buyers and will significantly impact the car’s value.

For more information on vehicle titles and branding, you can check resources like the USA.gov page on vehicle titles, which details how titles work across the United States.

4. Dealerships vs. Private Sales

Selling to a dealership might offer a simpler transaction, as they are experienced in handling various vehicle conditions. However, they may offer you a lower price due to the complexities the claim introduces. Private sales allow for potentially higher prices but require more effort and transparency from your side.

5. Paperwork and Lien Releases

Ensure all paperwork is in order. If there was a loan on the car, make sure you have a lien release from the lender once the loan is paid off (either by you or the insurance company).

6. Valuation Tools

Before you even approach buyers, get an idea of your car’s value. Use resources like Kelley Blue Book (kbb.com) or Edmunds (edmunds.com) to understand its market value, both before and after considering the claim or repairs. This will help you set realistic expectations.

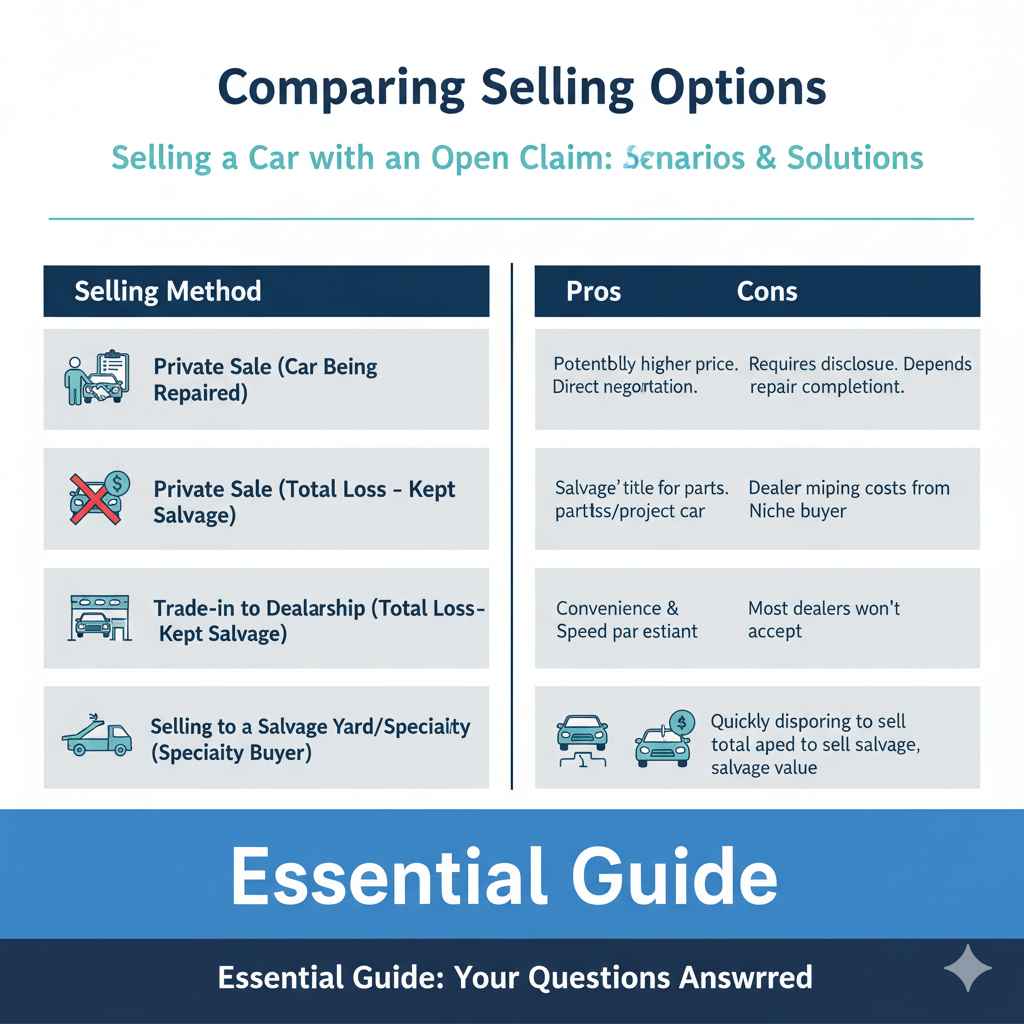

Comparing Selling Options

Let’s look at how different selling scenarios might play out when dealing with an open claim:

| Selling Method | Pros | Cons | Best For |

|---|---|---|---|

| Private Sale (Car Being Repaired) | Potentially higher selling price. Direct negotiation. | Requires significant disclosure and buyer education. Sale might depend on repair completion. | Sellers wanting maximum value and willing to be transparent about ongoing repairs. |

| Private Sale (Total Loss – Kept Salvage) | Can still sell the car for parts or project. | Must legally disclose “salvage” title. Significantly lower value. Buyer unlikely to be a typical driver. | Sellers who received a total loss payout, kept the salvage, and want to recoup some costs from parts or a project car. |

| Trade-in to Dealership (Car Being Repaired) | Simpler process. Dealer handles paperwork. | Lower trade-in value than private sale. Dealer might be hesitant due to ongoing repairs. | Sellers prioritizing convenience and speed over maximizing profit. |

| Trade-in to Dealership (Total Loss – Kept Salvage) | Dealer might take it for parts, but unlikely. | Very low value. Most dealers won’t accept salvage-titled vehicles as trade-in. | Rarely an option; usually better to sell salvage privately or to a salvage yard. |

| Selling to a Salvage Yard/Specialty Buyer (Total Loss) | Quickest way to get rid of a total loss vehicle. They handle towing. | Lowest payout. Only feasible if you kept the salvage. | Sellers who want to dispose of a total loss quickly and recoup some value from salvage. |

Frequently Asked Questions (FAQ)

Q1: Can I sell my car if it has an open insurance claim for damage, but it’s not a total loss?

A: Yes, you can, but you must be completely honest with potential buyers about the damage, the claim, and the repair status. You can either sell it as-is for a lower price, or wait for the repairs to be completed before selling.

Q2: What happens if my car is declared a total loss and the insurance company has paid me?

A: Once the insurance company pays you the agreed-upon settlement for a total loss, they typically take ownership of the damaged vehicle. You cannot sell it to anyone else because it’s no longer yours. You’ll need to surrender the title to them.

Q3: Do I have to tell a buyer about an accident my car was in, even if the claim is closed?

A: While not strictly an “open claim,” in most places, you are required to disclose significant accident history, especially if it resulted in major damage or the car was declared a total loss. Always err on the side of full disclosure to avoid legal issues.

Q4: Can I sell my car if the insurance company owes me money for repairs but hasn’t paid yet?

A: This can be tricky. If the insurance company is obligated to pay for repairs that haven’t been done, you’ll need to coordinate with them. You might sell the car with the understanding that the buyer will deal with the outstanding repair payment or the insurance payout directly, which can be complex.

Q5: Will an open claim affect my ability to get a clear title?

A: If repairs are ongoing for non-total loss damage, and the insurer is paying the repair shop or you directly, you should still be able to get a clear title once the work is done and all bills are paid. However, if the car is declared a total loss, the title will be branded as “salvage” if you retain the vehicle after receiving a payout.

Q6: What if I have a lien on my car, and it’s declared a total loss?

A: If your car has a lien (you owe money on it), the insurance company will pay off your loan directly to the lender as part of the total loss settlement. They will then take possession of the vehicle. You will receive any remaining settlement amount after the loan is paid.

Q7: Are there specific legal requirements for disclosing an open claim when selling a car?

A: Laws vary by state, but generally, sellers have a responsibility to avoid fraudulent misrepresentation. Not disclosing material facts about the vehicle’s condition, like an open total loss claim where ownership is disputed or salvage status, can lead to liability. It’s always best to follow the principle of caveat emptor (buyer beware) by providing all relevant information.

Conclusion

Selling your car with an open insurance claim might seem daunting, but it’s a manageable process when approached with honesty and clear communication. Whether your vehicle is heading for repairs or has been deemed a total loss, understanding your rights, responsibilities, and the specifics of your insurance policy is paramount. By disclosing the claim status transparently to potential buyers, coordinating closely with your insurance company, and ensuring all documentation is in order, you can navigate this situation effectively. Remember, as your automotive guide, my advice is always to prioritize clarity and integrity. This will not only protect you legally and financially but also ensure a smoother transaction for everyone involved, giving you peace of mind as you move on from your current vehicle.