How To Find A Cosigner For A Car Loan (Step-By-Step)

Finding a cosigner for a car loan means asking someone else to agree to pay the loan if you can’t. This person needs good credit. They also need to trust you. The process involves clear communication and understanding everyone’s risks. It’s about building a bridge to car ownership.

What is a Cosigner and Why Might You Need One?

Think of a cosigner as a safety net for the lender. They are a second person who signs the loan contract. This person promises to pay the car loan.

They do this if you miss payments or can’t pay at all. Your lender agrees to give you the loan. They do this because the cosigner’s good credit reduces their risk.

It’s a big favor to ask. They are putting their own credit on the line.

You might need a cosigner for a few big reasons. Your credit history might be short. Maybe you have a low credit score.

Perhaps you’ve had past financial problems. Even if you have a job, lenders look at your credit report. It tells them your history with money.

A cosigner can help bridge the gap. They show the lender you have a stronger chance of paying the loan back.

Many people think a cosigner is just for young folks. That’s not true. Anyone with a less-than-perfect credit score might need one.

It could be someone who is new to the country. It could be someone recovering from a bankruptcy. Sometimes, even someone with a decent score might need one.

This happens if they want a better interest rate. Or maybe they need a larger loan amount. The goal is to get approved.

The cosigner makes that possible.

Who Can Be a Cosigner?

This is a crucial question. Not just anyone can cosign a loan. The person you ask must meet specific requirements.

They need to have a good credit score. This is the main thing lenders look for. A good credit score shows they manage debt well.

They also need a stable income. The lender wants to know they can afford the payments. This is true even if you pay on time.

They have to prove they can handle the loan.

The ideal cosigner is someone you have a strong relationship with. This could be a parent, a spouse, or a close relative. Sometimes, a very trusted friend might agree.

It’s important that this person understands what they are agreeing to. They are taking on a significant financial responsibility. They are not just signing a paper.

They are making a promise to the bank.

Think about their financial situation. Are they already carrying a lot of debt? Do they have other loans or mortgages?

A lender will look at their debt-to-income ratio. This is how much debt they have compared to their income. If it’s too high, they might not qualify as a cosigner.

They also need to be willing. Asking someone is a big deal. It can strain relationships if not handled well.

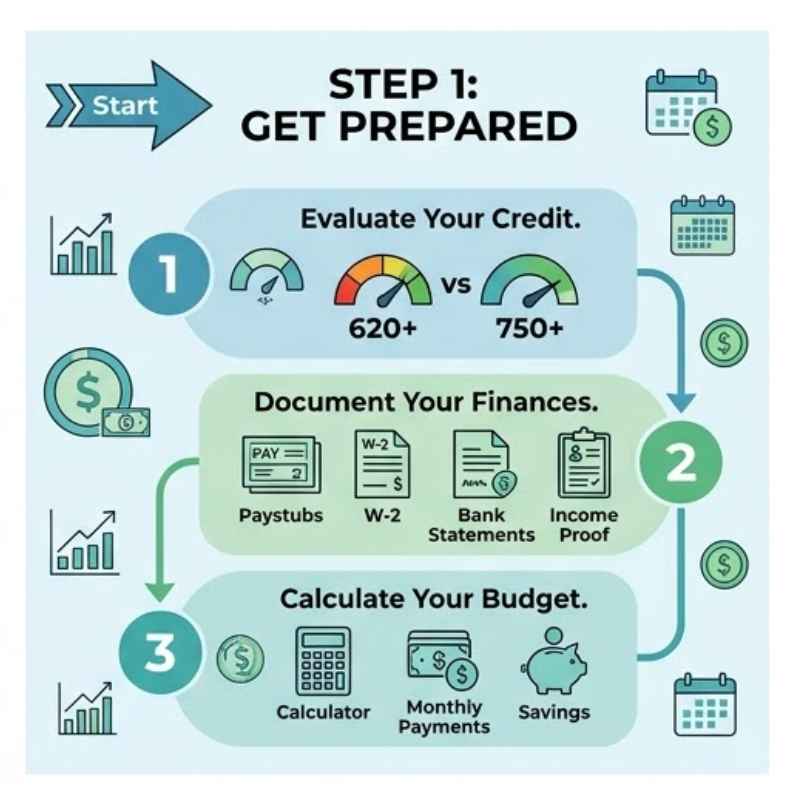

Step 1: Assess Your Own Financial Situation

Before you even think about asking someone, look at yourself. Why do you need a cosigner? What is your credit score?

You can get free credit reports. Check them for errors. Fix any mistakes you find.

This can boost your score a little. Understand your income. Is it stable?

Do you have a budget? Knowing these things helps you explain your situation. It shows you are serious.

How much car can you truly afford? Don’t just focus on getting approved. Focus on getting a loan you can manage.

A car payment is just one cost. You also have insurance, gas, and maintenance. These add up.

Make sure your budget can handle it all. Being realistic now saves problems later.

It’s also good to know the loan terms you want. What interest rate are you hoping for? What is the maximum loan amount?

Having this information ready makes you look prepared. It shows the potential cosigner you’ve done your homework. They will feel more comfortable helping you.

Your Credit Score Matters

What it is: Your credit score is a number. It shows how well you manage money. Lenders use it to guess how likely you are to pay back loans.

Why it’s key: A higher score means lower risk for lenders. This leads to better loan terms for you.

Action: Check your score for free. Work on improving it before you ask for a loan.

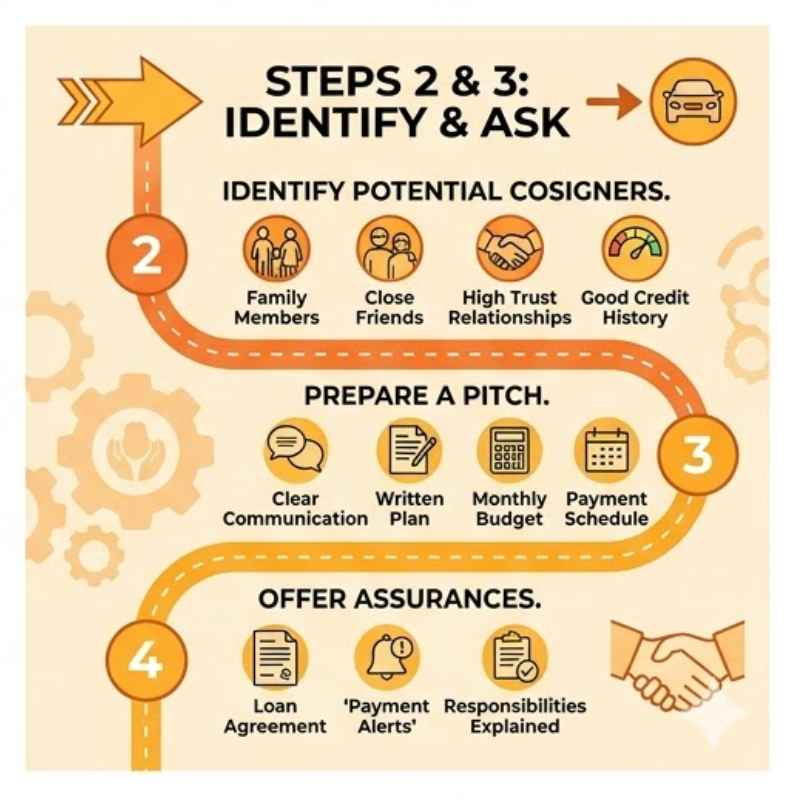

Step 2: Identify Potential Cosigners

Now comes the direct part. Who are the people in your life with good credit? Who trusts you enough to take this step?

Start with your closest family. Parents are often the first thought. Siblings, aunts, or uncles might also be options.

Think about spouses or partners too. They have a vested interest in your financial well-being.

Consider close friends. Is there a friend who is very financially responsible? Do you have a deep, trusting relationship?

This is a big ask for a friend. Make sure you value their friendship. You don’t want to damage it over a loan.

They need to have a good credit score and a steady income. This is non-negotiable for them to be able to help.

Be practical. Who in your life has shown good financial sense? Who do you trust deeply?

Who do you believe would help you if they could? List these people out. Think about each person’s financial situation.

Do they have other major debts? Are they retired? This helps you narrow down the list.

It’s also smart to have more than one potential person in mind. Sometimes, the first person you ask might not be able to help. They might have too much debt already.

Or they might have their own financial goals that prevent them. Having backups makes the process less stressful.

Step 3: Have an Open and Honest Conversation

This is perhaps the hardest part for many. You need to talk to them directly. Don’t beat around the bush.

Start by explaining your situation. Be clear about why you need a car and why you can’t get the loan alone. Share your credit score if you feel comfortable.

Explain what you have done to improve it.

Then, state clearly that you are asking them to be your cosigner. Explain what that means. Detail their responsibilities.

Emphasize that you plan to make every payment on time. Explain your budget. Show them how you will afford the car.

Share the loan details you are hoping for.

Listen to their concerns. They will have questions. They might worry about their credit.

They might worry about how it affects their borrowing power. Answer them honestly and patiently. Reassure them that you are committed to making this work.

Tell them about the car you are looking at. Mention its safety features and how it will help you.

It’s vital to be prepared for a “no.” They have the right to refuse. They are protecting their own financial future. If they say no, thank them for listening.

Don’t pressure them. Respect their decision. This is when having a backup person on your list is a lifesaver.

Cosigner Responsibilities Explained

Payment: The cosigner must pay the loan if you don’t.

Credit Impact: The loan appears on their credit report. It affects their credit score.

Risk: If you default, their credit takes a big hit. They may owe the full amount.

Your Role: You are the primary borrower. You are expected to make all payments.

Step 4: Research Lenders and Car Options

Not all lenders are the same. Some are more willing to work with cosigners. Dealerships often have financing departments.

Banks and credit unions are other options. Look for lenders who advertise “bad credit car loans” or “bad credit auto financing.” Read the fine print. See if they allow cosigners.

Compare interest rates and terms. Even with a cosigner, you want the best deal. Get pre-approved if possible.

This means a lender looks at your situation beforehand. It gives you a better idea of what you can afford. It also shows the car dealership you are a serious buyer.

When you look at cars, consider reliability and cost of ownership. A fuel-efficient car saves money on gas. A car with good safety ratings is important.

Make sure the car’s price fits your budget. Don’t overspend. Your cosigner is relying on you to be smart about this.

Buying a car that’s too expensive puts them at greater risk.

Think about the age of the car. Newer cars often have better financing options. But they also cost more.

Older cars are cheaper but might need more repairs. Balance what you can afford with what you need. A trusted mechanic can inspect a used car before you buy it.

This helps avoid costly surprises down the road.

Quick Loan Comparison Points

Interest Rate (APR): The yearly cost of borrowing money.

Loan Term: How long you have to pay back the loan (e.g., 36, 48, 60 months).

Down Payment: Money you pay upfront. A larger down payment can lower your loan amount.

Monthly Payment: The fixed amount you pay each month.

Step 5: Prepare Loan Application Documents

Once you have a lender and a car in mind, it’s time for paperwork. You and your cosigner will need to provide information. This typically includes proof of income.

Pay stubs, W-2 forms, or tax returns are common. You’ll need your driver’s license. Proof of address, like a utility bill, might also be needed.

Your cosigner will go through a similar process. They will need to provide their financial information. Their credit history will be checked.

The lender wants to see that both of you are good candidates for the loan. Be organized. Having all documents ready speeds things up.

Fill out the application carefully. Double-check all the information. Errors can cause delays or even lead to rejection.

Be honest about your income and expenses. Lenders verify this information. Making false statements can have serious consequences.

It’s a good idea to have a copy of the car’s purchase agreement. This shows the lender exactly what you are buying. It includes the make, model, year, and price.

This helps them assess the value of the collateral.

Step 6: Navigate the Loan Approval Process

This is where everything comes together. You and your cosigner will submit the application. The lender reviews all the information.

They look at your creditworthiness. They also assess the cosigner’s ability to pay. They will check the car’s value to ensure it matches the loan amount.

There might be a period of waiting. The lender might ask for more documents. They might call you or your cosigner with questions.

Be responsive. Promptly providing any requested information helps move the process along.

Once approved, you’ll receive the loan terms. Read them very carefully. Make sure you understand everything.

This includes the interest rate, the loan term, and the total amount you will repay. If something doesn’t look right, ask questions. Don’t sign anything you don’t fully understand.

If the loan is denied, don’t get discouraged. Ask the lender for the reason. Understanding the denial can help you improve your situation for the future.

Maybe you need to save for a larger down payment. Or perhaps you need to work on your credit more.

Credit Report Check-up

What it is: A detailed history of your borrowing and repayment habits.

What to look for: Errors, late payments, accounts you don’t recognize.

Where to get it: AnnualCreditReport.com offers free reports from Equifax, Experian, and TransUnion.

Real-World Context: The Car Dealership Experience

I remember helping my younger cousin find a car. He had just started his first real job. His credit was nonexistent.

He was excited but nervous. We went to a local dealership. The finance manager looked at his application.

He shook his head. “We can’t approve this on his own,” he said.

That’s when I stepped in. I had good credit and a stable job. I explained that I would cosign.

The finance manager’s whole demeanor changed. He was friendly and helpful. He pulled out different loan options.

He explained the interest rates and monthly payments. We looked at a few reliable sedans. He pointed out a car that was safe and within our budget.

It was a much smoother process. But I knew the weight of responsibility I was taking on. I had to be sure he could handle it.

Dealerships often have a whole team dedicated to financing. They work with many lenders. This can be very convenient.

They know which lenders are more flexible. They can also present your application in the best possible light. However, always be aware of the interest rates.

Sometimes, the convenience comes at a higher cost. It’s always a good idea to get a second opinion from your bank or credit union.

The car itself is part of the context. Lenders see the car as collateral. If you don’t pay, they can repossess it.

So, the car’s value matters. A lender won’t approve a loan for an expensive car if your income doesn’t support it. They also won’t approve it if the car is very old or has many miles.

This is why choosing a practical car is often the best route. It makes both you and the lender feel more secure.

What This Means for You: Managing Expectations

Having a cosigner is a huge help. It opens doors that might otherwise be closed. But it’s not a magic wand.

You still need to be responsible. Your cosigner is counting on you. Their credit is on the line.

When is it normal to need a cosigner? It’s common if you’re young. It’s common if you have no credit history.

It’s also normal if you’ve had financial struggles in the past. The important thing is that you are trying to rebuild. You are taking steps to improve your situation.

When should you worry? Worry if the loan terms are extremely bad. Are the interest rates astronomically high?

Is the repayment period incredibly long? This might mean the lender is taking advantage of your situation. Always compare offers.

Don’t accept the first thing you’re given.

A simple check is to look at the total amount you’ll pay back. Multiply your monthly payment by the number of months. Add any fees.

Does this total seem fair for the car you’re buying? If it seems way too high, it’s a red flag. Also, talk to your cosigner.

Are they comfortable with the terms? Their opinion is important.

Myth vs. Reality: Cosigner Edition

Myth: The cosigner owns the car.

Reality: You are the primary owner. The cosigner is only responsible for payments if you fail.

Myth: You can just ask anyone.

Reality: The cosigner needs good credit and stable income. It’s a big commitment.

Myth: The loan doesn’t affect the cosigner’s credit.

Reality: The loan is on their credit report. On-time payments help their credit; late payments hurt it.

Quick Tips for Finding a Cosigner

Here are some things that can help make the process smoother.

- Be Prepared: Know your credit score and budget before you ask.

- Ask Early: Don’t wait until the last minute. Give people time to consider.

- Be Clear: Explain exactly what being a cosigner means.

- Show Gratitude: Thank them profusely. Offer to help them in return.

- Make Payments On Time: This is the MOST important thing you can do. Prove you are reliable.

- Communicate: Keep your cosigner updated on your payments. Let them know you appreciate them.

These small steps show respect. They build trust. They make the cosigner feel good about their decision to help you.

It’s a partnership. You need to act like it.

Frequently Asked Questions

Can I be a cosigner for someone if I have bad credit?

No, typically you cannot be a cosigner if you have bad credit. Lenders require cosigners to have good credit. This is because the cosigner’s credit is used to guarantee the loan.

If your own credit is poor, you don’t offer the lender much assurance.

How long does a cosigner stay on the car loan?

A cosigner is on the loan for its entire duration. However, you can often refinance the loan later. You can do this once your own credit has improved.

Refinancing can remove the cosigner from the loan. This relieves them of their obligation.

What happens if I miss a payment and have a cosigner?

If you miss a payment, the lender will likely contact both you and your cosigner. The cosigner is then obligated to make the payment. If neither of you pays, it will negatively affect both of your credit scores.

This can lead to serious financial trouble.

Can a cosigner buy the car from me later?

Yes, a cosigner can sometimes buy the car from you. This would involve a separate sale agreement. They would also need to handle paying off the existing loan.

This is a complex situation. It requires careful legal and financial planning.

Will a cosigner help me get a lower interest rate?

Yes, having a cosigner with good credit often helps you get a lower interest rate. The lender sees less risk. This allows them to offer you better terms.

It can save you a lot of money over the life of the loan.

What if my cosigner wants to be removed from the loan?

It is very difficult to have a cosigner removed from a loan. The lender sees them as fully responsible. The only common way is to refinance the loan in your name alone.

This requires you to qualify on your own. You’ll need to show improved credit and income.

Conclusion

Finding a cosigner for a car loan is a process. It requires planning, honesty, and respect. By understanding the role of a cosigner and following these steps, you can increase your chances of success.

Remember to always be responsible. Your cosigner is doing you a big favor. Show them your appreciation through reliable payments.

You can achieve your goal of owning a car.