Is 800 Too Much For Car Payment? Essential Guide

An $800 car payment can be too much for many budgets, especially if it strains your ability to cover other essential expenses. It’s crucial to evaluate your income, debts, and lifestyle to determine if this monthly cost is sustainable and aligns with your financial goals and overall stability.

Buying a car is exciting! But so is making sure you can comfortably afford it. Many people wonder, “Is $800 too much for a car payment?” It’s a common question, and the answer isn’t a simple yes or no. Your personal finances are unique, and what one person can handle easily might be a struggle for another. We’re here to break down exactly how to figure this out for your situation so you can drive away with peace of mind, not financial stress. Let’s dive in and find clarity together!

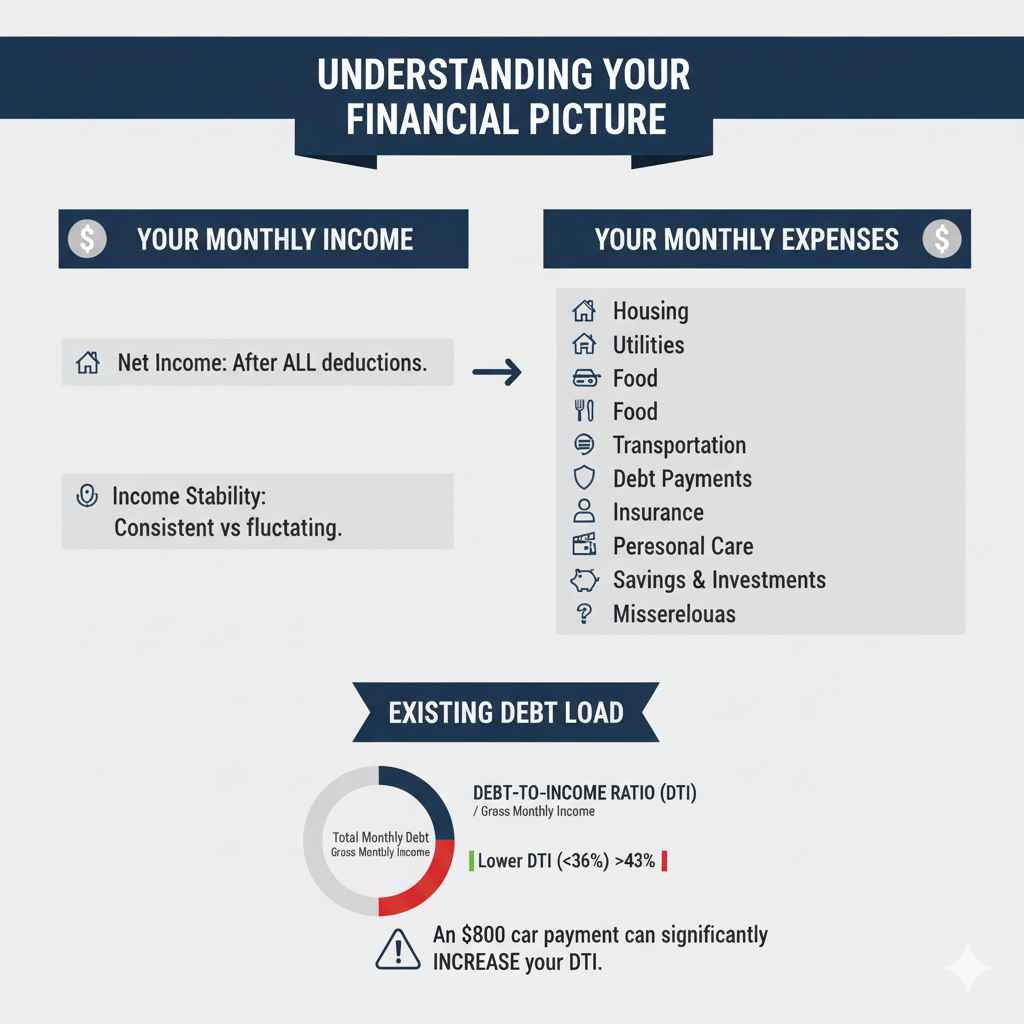

Understanding Your Financial Picture

Before diving into specific numbers, it’s vital to get a clear picture of your overall financial health. This isn’t about judging your spending; it’s about honest assessment so you can make the best decision for your wallet. Think of it like checking your tire pressure before a long trip – it ensures a smoother, safer journey.

Your Monthly Income

This is the foundation of your budget. We’re talking about your take-home pay – the money that actually lands in your bank account after taxes and other deductions. It’s important to be realistic here. Do you have a steady income, or does it fluctuate? Knowing this will help you determine how much wiggle room you truly have.

- Net Income: This is your income after all deductions. It’s the money you have available to spend.

- Income Stability: Is your income consistent month to month, or does it vary? This impacts how much risk you can take on.

Your Monthly Expenses

This is everything else you spend money on regularly. It’s helpful to list them all out. Don’t forget the small things, as they can add up quickly! Think about fixed costs (like rent or mortgage, which are usually the same each month) and variable costs (like groceries or entertainment, which can change).

- Housing: Rent or mortgage payments, property taxes, homeowner’s insurance.

- Utilities: Electricity, gas, water, internet, phone.

- Food: Groceries and dining out.

- Transportation: Gas, insurance (separate from car payment), public transit, maintenance, parking.

- Debt Payments: Student loans, credit card minimums, personal loans, existing car payments.

- Insurance: Health, life, renters/homeowners, etc.

- Personal Care: Haircuts, toiletries.

- Entertainment & Hobbies: Movies, dining out, gym memberships, hobbies.

- Savings & Investments: Contributions to retirement, emergency funds, other savings goals.

- Miscellaneous: Any other recurring or occasional expenses.

Existing Debt Load

High levels of existing debt can make adding another large payment very difficult. Lenders often look at your Debt-to-Income Ratio (DTI) to assess your ability to handle more borrowing. A lower DTI generally means you have more financial flexibility.

Your DTI is calculated by dividing your total monthly debt payments by your gross monthly income. For example, if your total monthly debt payments are $1,000 and your gross monthly income is $4,000, your DTI is 25% ($1,000 / $4,000).

Generally, a DTI below 36% is considered good. Lenders often prefer it to be below 43% to approve a loan, but the lower, the better for your financial comfort. An $800 car payment can significantly increase your DTI.

The “Is 800 Too Much For Car Payment?” Calculation

Now that you have a clear view of your financial landscape, let’s get to the heart of the matter. How do you really know if $800 is too much? There are guidelines and rules of thumb that can help you decide.

The 20/4/10 Rule

This is a popular guideline designed to help car buyers make smarter financial decisions. It’s simple to remember and apply:

- 20: Aim for a 20% down payment on your car. This means for an $800 monthly payment, the total car price might be higher, and you’d need to make a substantial initial payment.

- 4: Finance your car for no more than 4 years (48 months). Longer loan terms mean you pay more interest over time and might be “upside down” on your loan (owing more than the car is worth) for longer.

- 10: Your total monthly car expenses (payment, insurance, fuel) should not exceed 10% of your gross monthly income.

Let’s apply the 10% rule. If your gross monthly income is $8,000, then 10% would be $800. Based on this rule, an $800 car payment might be acceptable if it’s the total car expense (payment + insurance + gas), and your income is high enough. However, if your gross income is lower, say $6,000, then 10% is $600, making an $800 payment clearly too much by this standard.

The “Affordable Car Payment” Calculator Method

A simple way to gauge affordability is to look at percentages of your net monthly income (your take-home pay). Many financial experts suggest that your total car expenses (payment, insurance, fuel) shouldn’t exceed 15-20% of your net monthly income. If your take-home pay is $4,000, that’s $600-$800 total for car expenses.

If the $800 payment is just the loan payment, and you still need to add insurance (which can be $100-$300+ for a newer, more expensive car) and fuel, you can see how quickly that exceeds a comfortable percentage of your net income.

Considering the Total Cost of Ownership

A car payment is just one part of the picture. Don’t forget these ongoing costs:

- Car Insurance: This can vary wildly based on the car’s value, your driving record, location, and coverage levels. Newer, more expensive cars often have higher insurance premiums.

- Fuel: How many miles do you drive, and what’s the car’s fuel efficiency?

- Maintenance and Repairs: Even new cars need oil changes, tire rotations, and eventually, repairs. Older cars can have higher repair bills.

- Registration and Taxes: Annual fees to register your vehicle.

- Parking: If you live or work in an area with paid parking.

What an $800 Car Payment Typically Looks Like

An $800 monthly car payment usually indicates a higher vehicle price, a longer loan term, or a higher interest rate. Let’s look at some scenarios.

Loan Scenarios (Illustrative Examples)

These are simplified examples. Actual loan terms, interest rates, and taxes can vary significantly.

| Loan Term (Months) | Interest Rate (APR) | Loan Amount | Estimated Monthly Payment |

|---|---|---|---|

| 60 months (5 years) | 6% | $35,000 | ~$690 |

| 60 months (5 years) | 8% | $32,500 | ~$800 |

| 72 months (6 years) | 7% | $33,000 | ~$800 |

| 84 months (7 years) | 6% | $32,000 | ~$800 |

Note: These are estimates using a standard auto loan calculator. They do not include taxes, fees, or the down payment. A loan amount of around $32,000-$35,000 over 5-7 years at typical interest rates will often result in an $800 payment.

As you can see from the table, an $800 payment can mean a loan term of 5, 6, or even 7 years, or a loan amount in the mid-$30,000s. Longer loan terms mean you’ll pay significantly more in interest over the life of the loan. Consider this resource from the Consumer Financial Protection Bureau (CFPB) for more details on understanding auto loans.

The Impact of Interest Rates

A higher Annual Percentage Rate (APR) means you pay more for borrowing money. If you have a lower credit score, you’ll likely be offered a higher APR, which pushes your monthly payment up for the same loan amount and term. Improving your credit score can save you thousands of dollars in interest over the life of a loan.

The Trap of Longer Loan Terms

While a 7- or 8-year loan (84 or 96 months) might make an $800 payment seem affordable, it’s a risky path. You’ll be making payments for a very long time, and the car will lose value much faster than you pay off the loan. This can leave you “upside down,” owing more on your loan than the car is worth, which is a difficult spot to be in if you need to sell or trade in the car.

When is an $800 Payment Potentially Okay?

For some individuals, an $800 car payment might be manageable. This typically applies to those with:

- High disposable income: If your income significantly exceeds your expenses, leaving plenty of room for a higher payment.

- Low existing debt: If you have minimal or no other debts, that $800 payment won’t overwhelm your budget.

- A very low total car expense: If the $800 is the total monthly cost including insurance and fuel, and your income is substantial.

- A strong understanding and plan for finances: You’ve carefully budgeted and know you can afford it without sacrificing essential needs or savings.

- A business use case: If the vehicle purchase is directly tied to a business that generates significant revenue and profit, offsetting the cost.

However, even in these situations, it’s wise to be cautious. Could that $800 be better used for investments, savings, or paying down other debts more aggressively?

When is an $800 Payment Definitely Too Much?

If any of the following apply to you, an $800 car payment is likely a red flag:

- Your net income is less than $4,000-$5,000 per month. This is a general guideline, but an $800 payment would be a significant chunk of your take-home pay.

- You have other significant monthly debt payments (student loans, credit cards, mortgages) that already consume a large portion of your income.

- You live paycheck to paycheck or have a very small emergency fund.

- The $800 is just the payment, and other car costs (insurance, gas) will add hundreds more.

- You’re stretching to afford the down payment or meet the loan’s down payment requirements.

- You’d have to cut back on essential spending (groceries, utilities, medical care) to make the payment.

- You don’t have clear visibility into your budget.

A good rule of thumb is the 10% rule for total car expenses (payment, insurance, gas) based on your gross income, or the 15-20% rule for total car expenses based on your net (take-home) income. If an $800 payment blows past these figures, it’s too much.

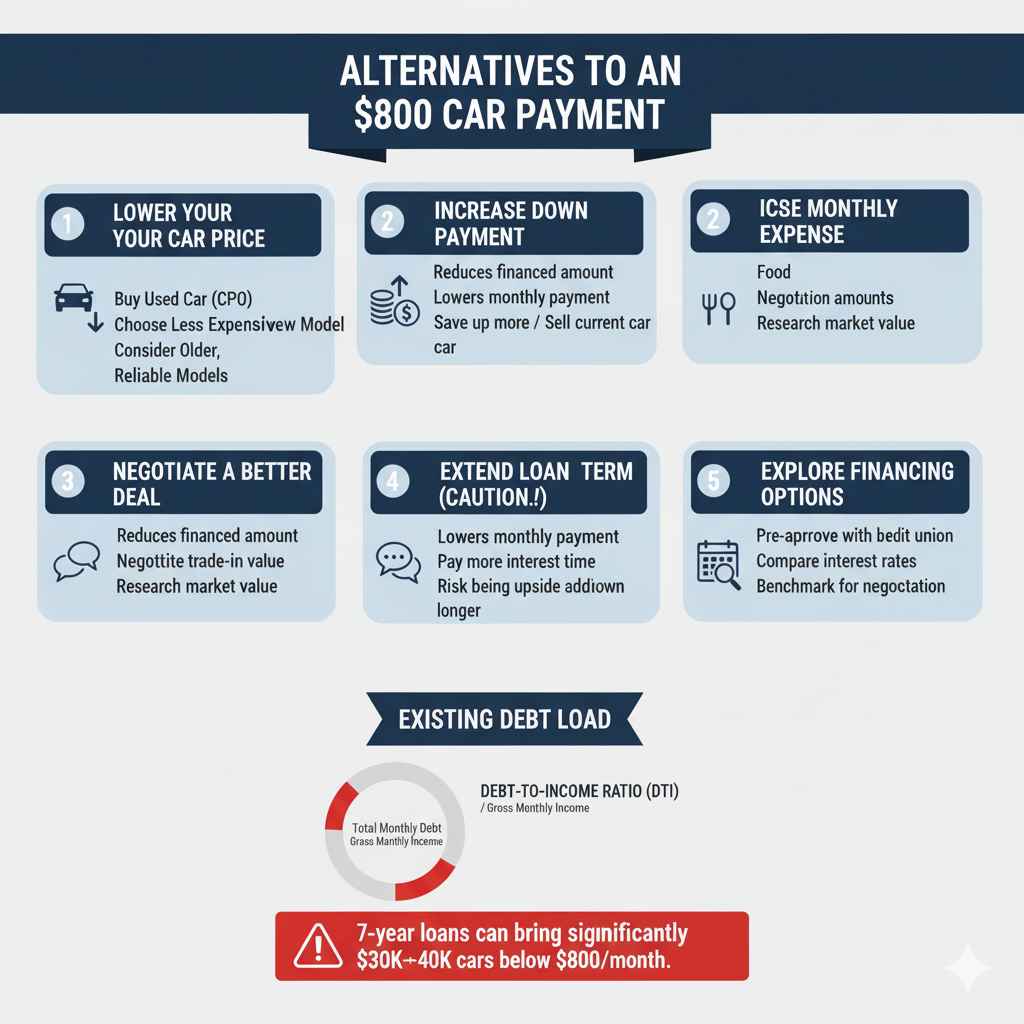

Alternatives to an $800 Car Payment

If $800 feels like too much, don’t despair! There are smart ways to get a reliable vehicle without breaking the bank.

1. Lower Your Expectations (and Your Car Price)

The most direct way to lower your payment is to choose a less expensive car. This could mean:

- Buying a Used Car: Certified Pre-Owned (CPO) vehicles or well-maintained used cars can offer significant savings. Check out resources like Edmunds’ used car listings for options.

- Choosing a Less Expensive New Model: Opt for a compact car, a smaller SUV, or a less optioned-out trim level of a vehicle you like.

- Considering Older, Reliable Models: Many cars are built to last. A well-maintained car that’s a few years older might be significantly cheaper to purchase and insure.

2. Increase Your Down Payment

A larger down payment reduces the amount you need to finance, directly lowering your monthly payments and the total interest paid. Can you save up more before buying? What about selling your current car?

3. Negotiate a Better Deal

Don’t be afraid to negotiate the price of the car, the trade-in value of your current vehicle, and the interest rate on your loan. Do your research beforehand on the fair market value of the car you’re interested in.

4. Extend Your Loan Term (with Caution)

While not ideal, a slightly longer loan term (e.g., 72 months instead of 60) can reduce the monthly payment. However, be aware that you’ll pay more interest over time, and you risk being upside down on the loan for longer. As seen earlier, 7-year loans often bring payments down below $800 for vehicles in the $30k-$40k range.

5. Explore Different Financing Options

Get pre-approved for a loan from your bank or credit union before you go to the dealership. They may offer better interest rates than dealership financing. This also gives you a benchmark for negotiation.

Frequently Asked Questions (FAQ)

Q1: What is a good monthly car payment percentage of income?

A generally accepted guideline is that your total monthly car expenses (payment, insurance, fuel) should not exceed 10% of your gross income or 15-20% of your net (take-home) income. Sticking to these numbers helps ensure you can comfortably afford your car without financial strain.

Q2: If my income is $100,000 per year, is $800 too much for a car payment?

If your gross income is $100,000 per year, that’s about $8,333 per month. The 10% rule suggests total car expenses shouldn’t exceed $833 per month. So, if your $800 payment is the only car expense, it might be okay. However, if you add insurance and gas, the total could exceed $833. It depends on your other financial obligations and lifestyle.

Q3: Should I worry if my car payment is over $500?

Whether a $500 payment is too much depends entirely on your income and expenses. If your net income is $3,000, a $500 payment (plus insurance and gas) is likely too much. If your net income is $7,000 and you have few other debts, $500 might be very manageable. Always compare it to your personal budget.

Q4: Is it bad to finance a car for 7 years?

Financing a car for 7 years (84 months) is generally not recommended. While it lowers your monthly payment, you’ll pay significantly more in interest over time. More importantly, your car will depreciate much faster than you pay off the loan, leaving you “upside down” for a long period. This means you owe more than the car is worth, making it difficult to sell or trade in.